The latest updates from Fathom’s Financial Vulnerability Indicator, which estimates the probability of sovereign, currency and banking crises, show increasing levels of sovereign risk, particularly in emerging market economies like India.

- Fathom’s Financial Vulnerability Indicator (FVI) provides a comprehensive assessment of sovereign, currency and banking risk for 176 countries and is available to Refinitiv customers via Datastream.

- The latest FVI reading shows a spike in the probability of a sovereign crisis in emerging market economies, reflecting slower global growth (as the effect of re-opening fades away), and tighter monetary policy.

- India is an example of where sovereign risk vulnerabilities are growing, with trade and financial market interlinkages making it more vulnerable to external developments.

For more data-driven insights in your Inbox, subscribe to the Refinitiv Perspectives weekly newsletter.

Financial crises are rare – they occur less than 1 percent of the time – and are undoubtedly very difficult to predict. Fortunately for those seeking to protect against them, they tend to be preceded by warning signs.

Combining the best of today’s modelling techniques with the lessons of the past enables us to highlight these flashing lights and identify mounting vulnerabilities before the market exposes them.

Modelling the past to predict the future

Mark Twain famously said that “history never repeats itself, but it does often rhyme”. That maxim is a guiding principle for Fathom’s Financial Vulnerability Indicator (FVI), which assesses the probability of banking, sovereign and currency crises countries on a quarterly basis for 176 countries.

The FVI’s identification of past crises is consistent with that of Laeven and Valencia (2020), who catalogued financial crises dating back to 1970. Fathom has modelled those past crises to quantify the relative importance of the factors driving each.

A history book is not sufficient, though – predicting future crises also requires using the best of today’s analytical tools and data.

One challenge outside of the advanced economies is the patchy quality and availability of data.

To address this, the FVI uses a machine-learning algorithm to fill gaps in the dataset. Rather than simply averaging across countries or dropping a country due to lack of coverage for certain series, the ‘k Nearest Neighbour’ approach assigns a proxy variable based on similarities to other countries. That means a richer, more comprehensive tool which does not compromise on data quality.

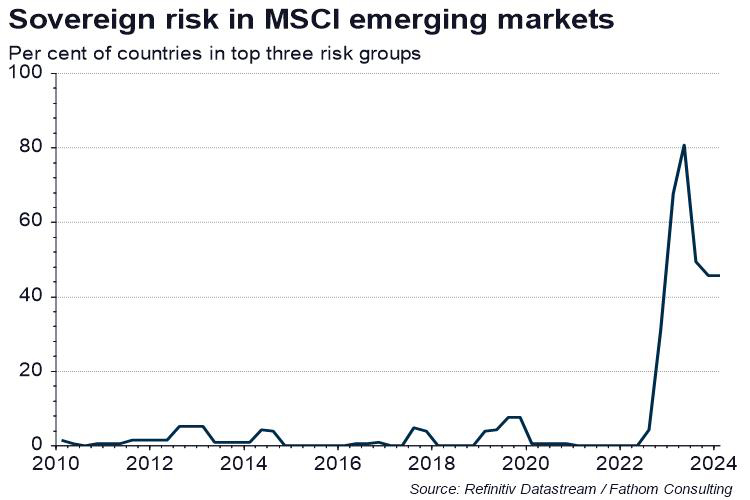

Sovereign risk in emerging markets

So, what is the FVI saying now? Zooming in on sovereign risk, the FVI currently identifies a historically high probability of that form of crisis occurring in emerging market economies, exceeding the levels observed during the Arab spring.

The FVI allows sovereign risks to be analysed in risk groups, aggregating countries that have similar chances of experiencing a crisis.

More than one-third of EMs are now in one of the top three risk groups, with at least a 1-in-25 chance of defaulting or restructuring their debt. In part, this reflects these countries’ exposure to the global slowdown in economic activity and the tightening of monetary policy.

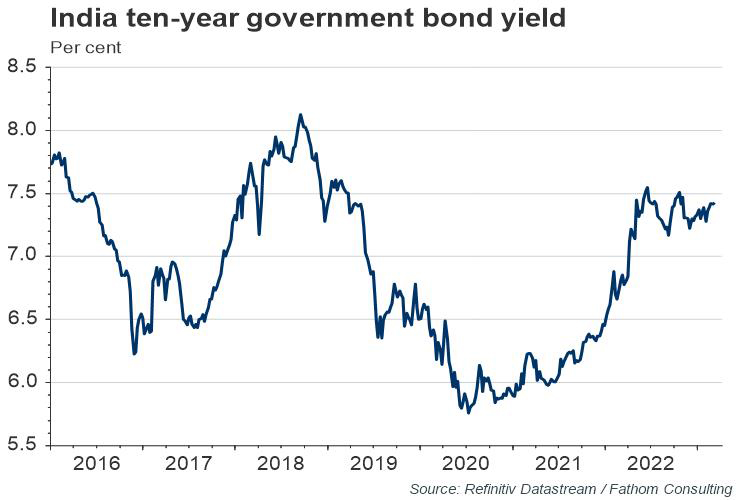

Is India at risk of default?

Where are those risks most likely to crystallise?

There has been much recent commentary on Pakistan’s prospects after its foreign exchange reserves rapidly depleted and the government began formal negotiations on a bailout with the IMF.

Much less, though, the FVI suggests sovereign risks are also building across the border in India.

On the domestic front, that is largely a feature of its rising bond yields.

The FVI emphasises sudden changes in macroeconomic and financial market variables and India’s ten-year yield rose sharply in 2021 and early 2022 after a period of gradually declining and stable yields.

In today’s financial system, no man is an island.

The FVI seeks to capture the impact of global developments, as well as contagion from events abroad. The more central a country is to global networks, the more it is impacted by external developments.

Those impacts can be particularly forceful when there are direct trade and market linkages to places where vulnerabilities are emerging.

With the United States and Europe accounting for more than 40 percent of Indian exports, weak growth and potential recessions in those economies may have a particularly strong impact on India in the year to come.

With its dependence on capital inflows, India is also vulnerable to contagion from higher bond yields abroad, with no sign yet of a return to the low-yield environment of the last decade.

On the plus side, India has low external debt compared with peers, and a healthy level of FX reserves, which will help it to sail through any choppy waters. The FVI will continue to monitor the waves.

Refinitiv customers can access the FVI via Datastream on an aggregate basis, with quarterly series available for all three types of crisis back to 2010. The aggregation is based on geographical regions, but also by income level and by IMF and MSCI categorisation.