With inflation running at multi-decade highs, a new report by Fathom Consulting assesses the cause of the problem and asks “what impact will this have on the upcoming U.S. midterm elections?”

- Inflation has repeatedly surprised to the upside over the past year as supply has failed to keep pace with surging demand. This is not just a U.S. problem; it is a global phenomenon.

- Households dislike inflation. We find evidence that higher inflation has roughly the same negative impact on household sentiment as an increase in the unemployment rate, a restatement of Arthur Okun’s ‘misery index’.

- Rampant inflation is likely to harm the Democratic Party’s chance in the upcoming midterms. Other non-economic factors (increasing bipartisanship and a historic bias against incumbent politicians) also reduce the chances of the party retaining control of both houses.

For more data-driven insights in your Inbox, subscribe to the Refinitiv Perspectives weekly newsletter.

What is happening with inflation?

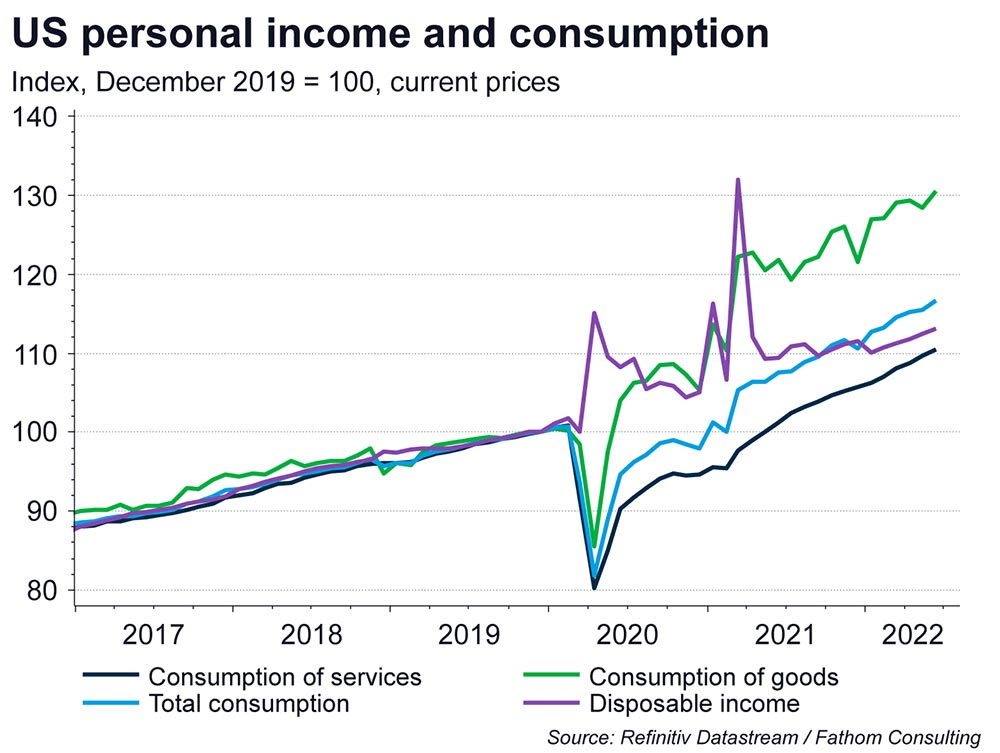

Refinitiv’s data helps us track both the causes and symptoms of the current inflation crisis. Its origins go back to the early days of the pandemic, when fiscal support ensured that U.S. household incomes rose despite the deepest global recession in recorded economic history.

That additional income has primarily been used to fund both an increase in consumption and a change in its composition — there has been a significant pivot away from the consumption of services and towards the consumption of goods.

The causes of the initial overshoot in inflation are therefore straightforward to understand — the supply side of the economy has struggled to keep pace with the increase in demand and its changing composition.

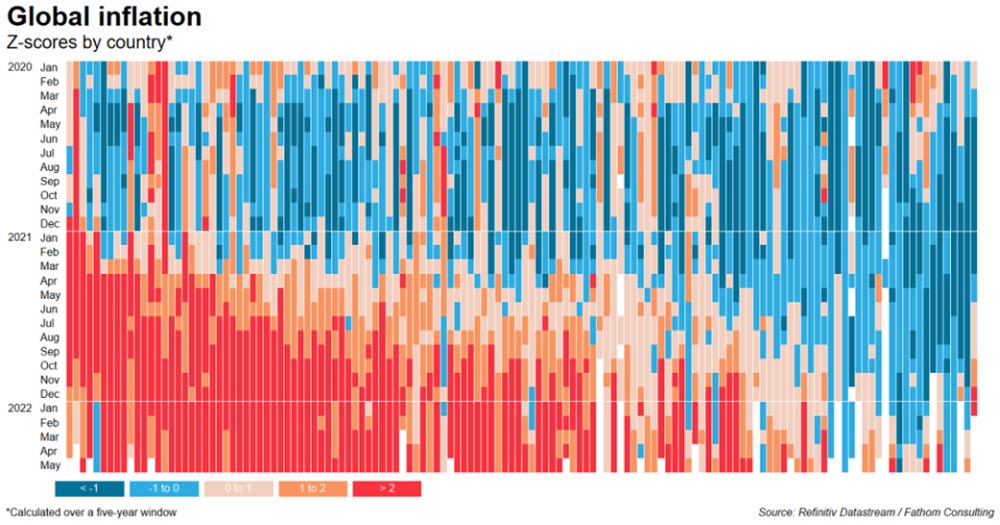

The inflation overshoot is not a uniquely U.S. phenomenon. The heatmap below shows 12-month inflation rates across 134 countries readily available from Datastream’s list of key indicators. These have been z-scored (i.e., adjusted to take account of each country’s usual rate of inflation and its typical volatility).

The red cells reflect outturns that are two standard deviations above normal — statistically, this represents an incredibly rare event. Most countries are now in this position.

What do households think about inflation?

The term ‘money illusion’ was coined by Irving Fisher in the early 20th century. Economists use it to capture the psychological phenomenon that people dislike inflation even if salary increases completely offset its impact.

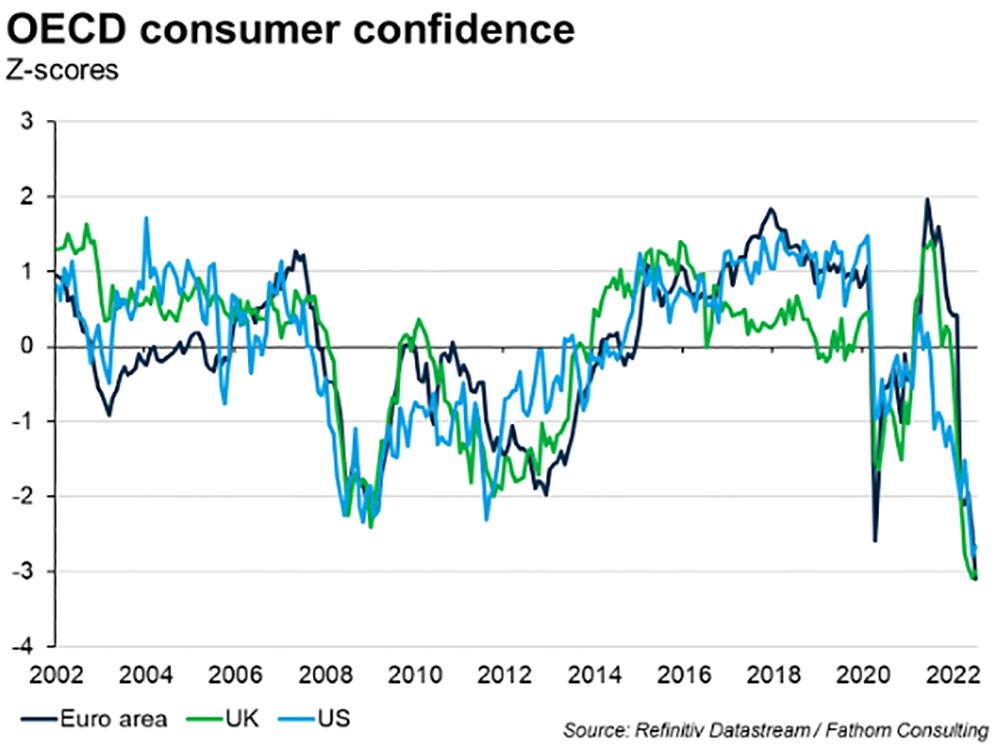

This outlook on the world implies that higher inflation can lead to a decrease in consumer spending and a precautionary increase in saving. This is clear to see in surveys of consumer sentiment — confidence in the U.S., the UK, and the euro area has fallen to levels that almost always signal an impending recession.

Fathom has tested empirically for further evidence of the relationship between inflation and household confidence.

We have found evidence that:

- Households react negatively to falling asset values (i.e., equity and house prices)

- Households respond negatively to higher inflation

- Households respond negatively to higher unemployment

- Households are roughly as sensitive to inflation as they are to unemployment

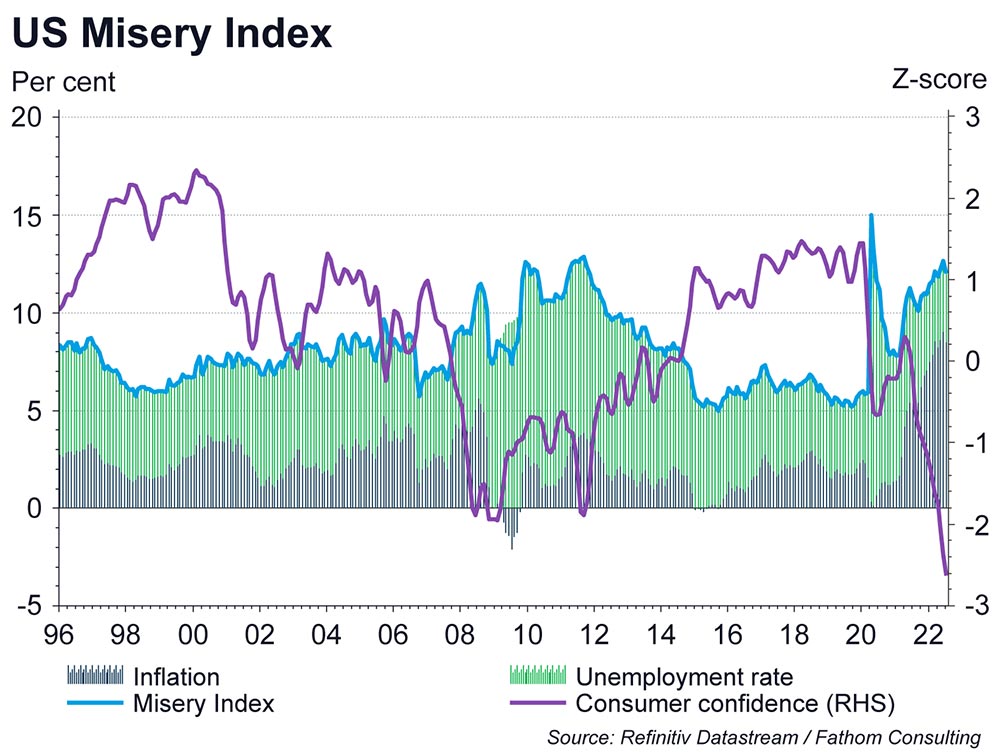

This last finding is especially intriguing since it lends empirical support to the ‘Misery Index’, which simply sums up inflation and the unemployment rate.

This empirical rule of thumb was developed by Arthur Okun, an economic advisor to President Johnson, as an indicator of ‘economic discomfort’. It is plotted below against consumer confidence.

What effect will this have on the U.S. midterms?

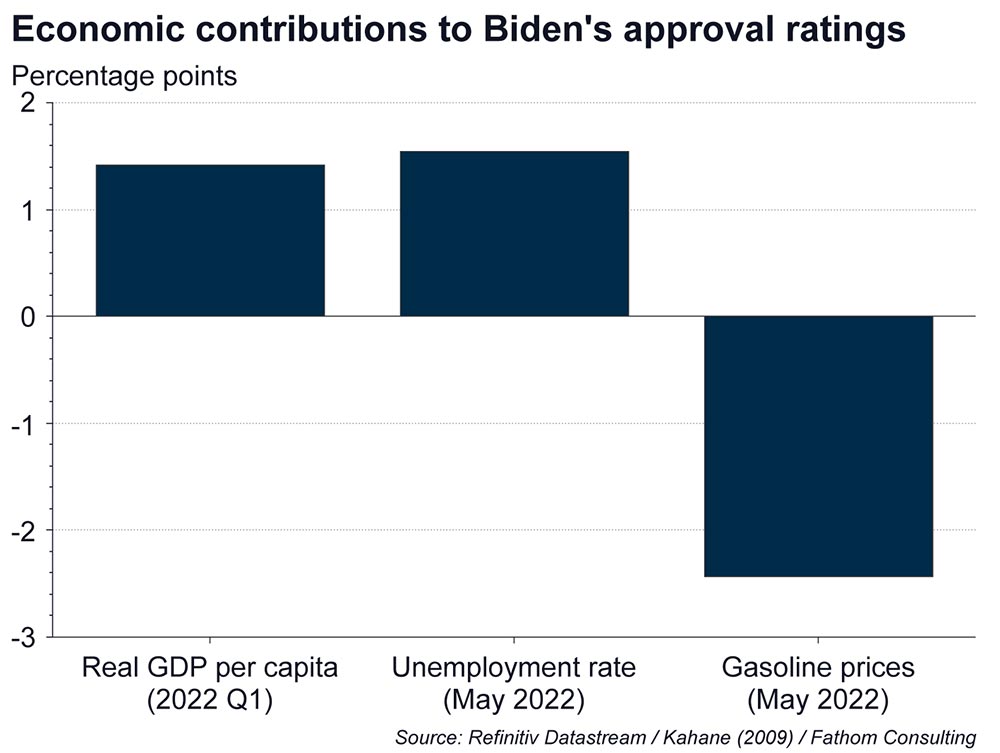

Americans are due to go to the polls later this year for midterm elections. Empirical work by Kahane (2009) attempted to quantify the impact of macroeconomic variables on U.S. election outcomes.

Combining the findings from that work with more recent data out-turns, leads to the conclusion that economic variables would still be expected to contribute positively to President Biden’s approval ratings, thanks to the strength of the post-COVID-19 recovery in GDP.

There are, however, other factors still at play.

First, bipartisanship is increasingly dominating U.S. politics implying that there are fewer swing voters now than in the past. (It is these swing voters who are more likely to vote according to economic issues.)

Second, there is typically a large swing against the incumbent president during midterm elections. Congressional voting records show that, since the end of World War II, the incumbent’s party has lost an average of 27 House seats and three Senate seats in midterm elections.

Given the Democratic Party’s wafer-thin majorities in both houses, there is a high chance that they will lose control of one, if not both, houses.

Interested in more?

This report highlights some of the key findings from a recent Fathom report. Please follow the link below to read the full paper and gain more insights on the inflation crisis including: the forecasting errors of economists; the implications for monetary policy; and further discussion of the political consequences of inflation.