Deal making activity in Asia Pacific (APAC) set all-time records in the first four months of 2021 in anticipation of a successful recovery from COVID-19.

- Deal making in Asia Pacific region is experiencing a boom in 2021 with investment banking fees hitting an all time high in Q1.

- In Q1 2021, M&A activity in APAC-ex Japan was up by 55 percent, reaching the highest level since 2015.

- Asia Pacific equity markets have also rapidly risen. Q1 2021 has made a record start with US$109.6bn raised.

For more data-driven insights in your Inbox, subscribe to the Refinitiv Perspectives weekly newsletter.

The high activity of deal making in APAC has been demonstrated by the spike in global and regional investment banking fees, which reached a record US$50bn, up 35 percent from a year earlier – an all-time high – as of April 2021.

In APAC, fees were up 21 percent year-to-date (YTD) from a year earlier to US$9bn, the highest since records began in 2000.

Whether this deal making bounty can continue will depend on how successful the region’s governments are in containing COVID-19 and fuelling a sustained economic rebound, according to insights shared by a panel of experts and a global audience of institutional investors attending a webinar hosted by Refinitiv in May 2021.

Mega deals on the march

The momentum in mega deals continued into the first quarter of 2021 with global M&A volume exceeding a trillion dollars for the third consecutive quarter. In APAC-excluding Japan, M&A activity was up 55 percent YTD to US$365bn, the highest YTD total since 2015.

Even mid-cap deals saw a 19 percent growth in value, meaning activity is not being propped up by the headline deals alone.

Deals involving Japan, meanwhile, were up 59 percent YTD to US$70bn, a record since 2018. Japan made its mark was in cross-border activity; taking China’s place as the world’s fourth biggest source of outbound M&A activity.

Between 2014 and 2018, China had moved aggressively into the cross-border M&A space. However after 2018, Chinese corporate deal making stayed home and cross-border deals dried up on the back of trade wars and rising protectionist sentiments.

Nonetheless, China remains the most attractive destination for private equity (PE) deals.

PE-backed deals in APAC reached an all-time high of US$54bn YTD, of which Chinese targets accounted for US$30bn. There were increases across the board, with smaller markets like Australia, India, Singapore and South Korea seeing triple-digit percentage increases.

Perhaps opportunities that were attractive before the pandemic have become even more so due to attractive valuations and the low interest rate environment.

Technology, with a 33.5 percent share, has been the biggest target for PE-backed M&A activity in APAC, the panelists noted. This comes as no surprise given the acceleration of digital transformation in the wake of the pandemic. Also benefiting from COVID-19 was the healthcare sector, which took a 10.6 percent share.

Deal making headlines

The biggest deal in APAC – as well as the biggest tech sector deal globally – was the Special Purpose Acquisition Vehicle (SPAC) merger of Singapore-based Grab Holdings and U.S.-based Altimeter Growth Corp, which values Grab at US$31.1bn.

Meanwhile, two Japanese technology giants, Hitachi and Panasonic, announced acquisitions of U.S.-based tech companies, pushing deal activity and driving record level of activity in the tech space.

At the same time, bricks and mortar activities also came into focus, with four deals in China’s cement industry accounting for acquisitions worth a combined US$18bn.

Equity capital markets

APAC equity markets have also been on a tear, with Q1 2021 marking a record start to a year with US$109.6bn raised across the region excluding Japan – a 134 percent increase.

Among the drivers of that boom are reforms in China that allow companies to raise money without having to go through time-consuming approval processes.

There have also been a few landmark issuances by South Korean companies this year.

SK Bioscience, a pharmaceutical company working on the rollout of COVID-19 vaccines, raised US$1.3bn from a domestic IPO. Electric vehicle battery maker SK IET became the country’s biggest IPO ever by raising US$2bn. And Coupang, the country’s answer to Amazon, became the biggest US IPO overall since Uber Technologies in May 2019.

Chinese listings in the U.S. “have continued despite political rumblings suggesting China companies would be kicked out of the main markets,” noted Steve Garton, Asia editor at IFR.

“The Hong Kong market has been a beneficiary of some of those changes in the U.S., with companies like Baidu coming back closer to home to list in Q1 through secondary listings.”

Other major deals so far this year in Hong Kong include a follow-on offering in Tencent by its South African major shareholder, Naspers, which sold a 2 percent stake for US$14.6bn. And Meituan raised US$10bn from the sale of shares and convertible bonds to build a war chest to fund technology development, including autonomous delivery vehicles and drones.

China and South Korea also dominate the Asia equity capital-raising pipeline pipeline, with jumbo equity issues slated for 2021, including Didi Chuxing, JD Logistics, LG Energy Solution, KakaoBank and several companies in the biotech sector. Hong Kong is expected to be the leading venue for those listings, with more Chinese companies able to list in the city as a result of market reforms.

“We also expect capital market reforms in China to open up a lot of opportunities for ECM fundraising there,” added Garton.

Is the SPAC boom over?

SPACs dominated U.S. IPO issuance in Q1, accounting for 75 percent of all listings and 69 percent of funds raised.

“From where we were this time last year, with a few deals going through but clearly only a small part of the market, we’ve raced up to over US$30bn of SPAC listings, raising money in the U.S. and then going out and trying to buy assets with those resources,” said Garton.

Although Asia Pacific lags far behind the U.S. SPAC trend, sponsors in the region have nevertheless raised over US$5.5bn since the start of 2021, including Hong Kong billionaire Richard Li’s Bridgetown 1 & 2, Singapore hedge fund guru Ray Zage’s Tiga and Hong Kong-based HH&L Acquisition.

Other big names in the region are also looking to launch SPACs but there are concerns that the SPAC wave heading towards APAC may be delayed as the U.S. Securities and Exchange Commission ponders the introduction of new investor protections measures.

“Unfortunately for all of them, the SEC is now looking into how these things work, and perhaps coming up with rules that will make it much harder for SPACs to raise money in future,” said Garton. “That has put the brakes on SPACs.”

However, it could be that when there is more clarity on long-term treatment of these SPAC formats by regulators, “it will get back up again,” according to Garton.

Debt issuances

Meanwhile, debt issuances have cooled after a strong start to the year.

“In January, with vaccines being rolled out, people were happy to take risks,” noted Garton. “February was a much quieter session because of volatility, with the 10-year U.S. Treasury rate going from below 1 percent at the start of the year to over 1.5 percent by April, making it difficult for people to plan when to come to market.”

A particular concern for debt markets in Asia is the continuing uncertainty around China Huarong, one of China’s four biggest distressed asset management companies.

“This has hit sentiment in the state sector in China, specifically, as well as more high-risk names. High yield has been hit by profit taking and people pulling back on risk,” Garton said.

Deal making prospects for 2021

With 2021 having begun with a bang in deal making, is there a chance it could go out with a whimper?

Much of the continued boom in deal making will no doubt depend on the pandemic’s trajectory, especially with the bullishness brought about by the rollout of vaccines partly dampened by the difficulty in getting populations vaccinated, either because of shortages or so-called “vaccine hesitancy”.

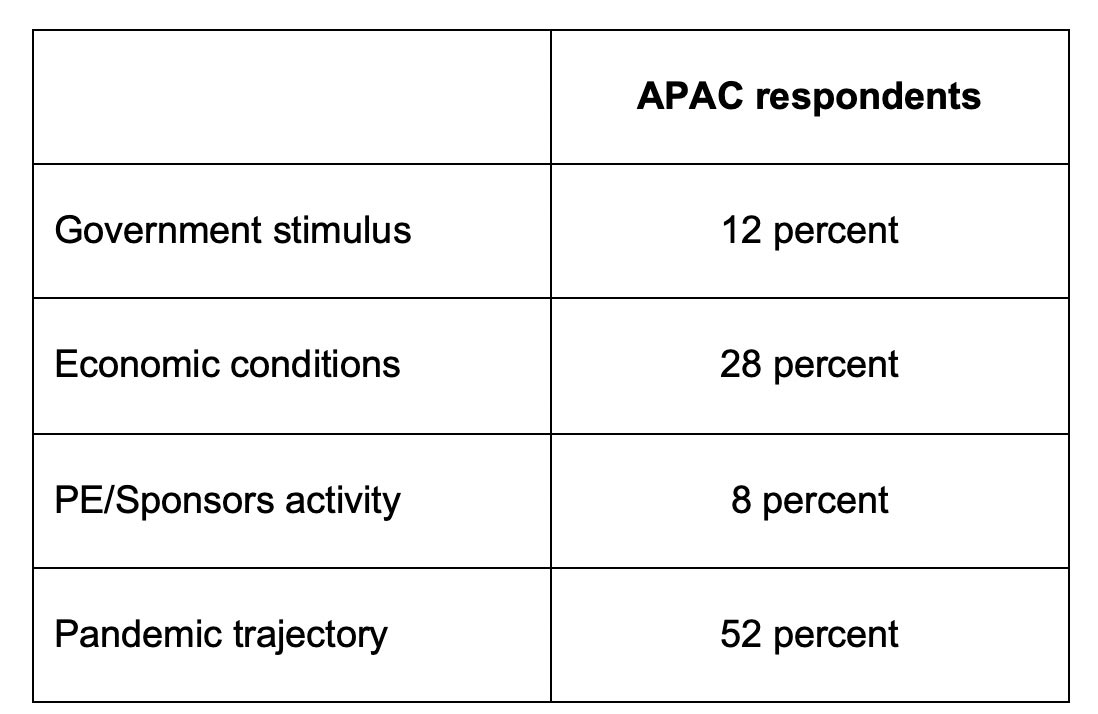

An audience poll at the beginning of the webinar found the majority of respondents believed the pandemic would have the biggest impact on overall corporate finance activity in 2021.

Which factors will have the most significant effect on the overall corporate finance activity in 2021?

Looking back, a year ago it was difficult to guess the incredible capital markets boom and record issuance we’ve seen over the last 12 months.

And Refinitiv’s latest Deal Makers Sentiment Survey of over 460 respondents found that optimism for 2021 is high, with most expecting M&A activity to register growth for the year, although they are also conscious of risk.

On average, the respondents predicted a 6 percent increase in activity this year globally, but judging by the performance and trajectory of deal activity so far, their expectations could well be comfortably exceeded once again.

In Asia, the recovery appears relatively immune to downsides and the outlook remains positive, given its nascent sustainable finance boom and formidable equity pipeline.

Discover Refinitiv Workspace

Designed with the future of investment banking in mind, and in a rapidly changing and competitive market, Refinitiv Workspace for Investment Bankers is a powerful, smart and customer-centric solution built precisely for deal professionals.

It integrates with your workflow and sharpens your edge through insights, speed and intuitive navigation bringing you the content and functionality you need.

Refinitiv Workspace enables you to find the content you need straight away.