We use the StarMine Sovereign Risk Model (StarMine SR) to analyse the development of the economic crisis in Sri Lanka, which caused the nation to default in May 2022.

- In May 2022, Sri Lanka defaulted, and is now seeking to restructure debts of more than $50bn it owes to foreign creditors.

- The StarMine Sovereign Risk provides robust estimates of the probability of default of sovereign nations over multiple time horizons, using a broad spectrum of data inputs.

- We analysed the last four years of the model output for Sri Lanka and found that the probability of default increased significantly in mid-2021, and at the beginning of 2022.

For more data-driven insights in your Inbox, subscribe to the Refinitiv Perspectives weekly newsletter.

The StarMine SR helps us to analyse the last four years of the model output for Sri Lanka, which defaulted on its sovereign debt in May 2022.

The StarMine SR calculates the probability of default (PD) within six different time horizons and assigns letter ratings based on the one-year PD. It also breaks down the risk into short- and long-term components which are percentile ranks over all countries scored, with values ranging from 1 to 100, where the value 1 represents the highest risk.

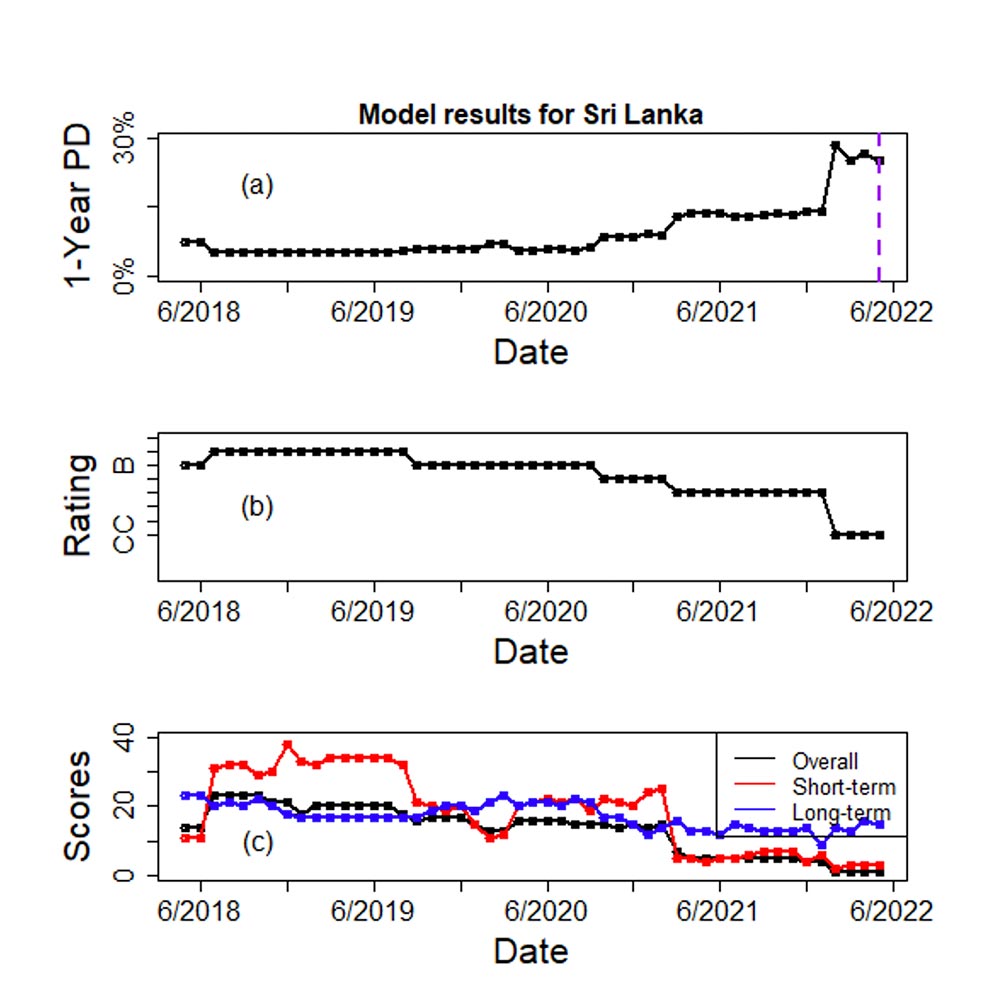

As shown in Figure 1(a), Sri Lanka had a 1-year PD of around 7 percent in the middle of 2018 and that grows over time.

Significant increases happen in the PD in mid-2021 and the beginning of 2022, most likely a reflection of the economic impact of the COVID-19 pandemic. Tourism, which traditionally was one of the main sources of foreign currency for Sri Lanka, crashed during the pandemic. Eventually, Sri Lanka defaulted in May 2022.

StarMine SR has classified Sri Lanka as junk grade (below BBB-) for several years, as shown in Figure 1(b), indicating a country with high risk of default.

Figure 1. Sri-Lanka 1-year probability of default (a), letter rating (b), overall, short- and long-term scores (c) as a function of time. The vertical broken line in (a) marks the default date.

Origins of Sri Lanka’s economic crisis

By studying the short- and long-term scores of the model, as shown Figure 1(c), one notices that the long-term score shows a fairly steady decrease over time. By its nature, the short-term component fluctuates more than the long-term component.

However, if long- and short-term scores both show low values, the overall score is also low, and this is an indication of a country in a crisis.

We can see that for most of the last four years, Sri Lanka has been in the bottom quintile for the overall, long- and short-term scores. In May 2022, its overall score was 1 – the lowest possible.

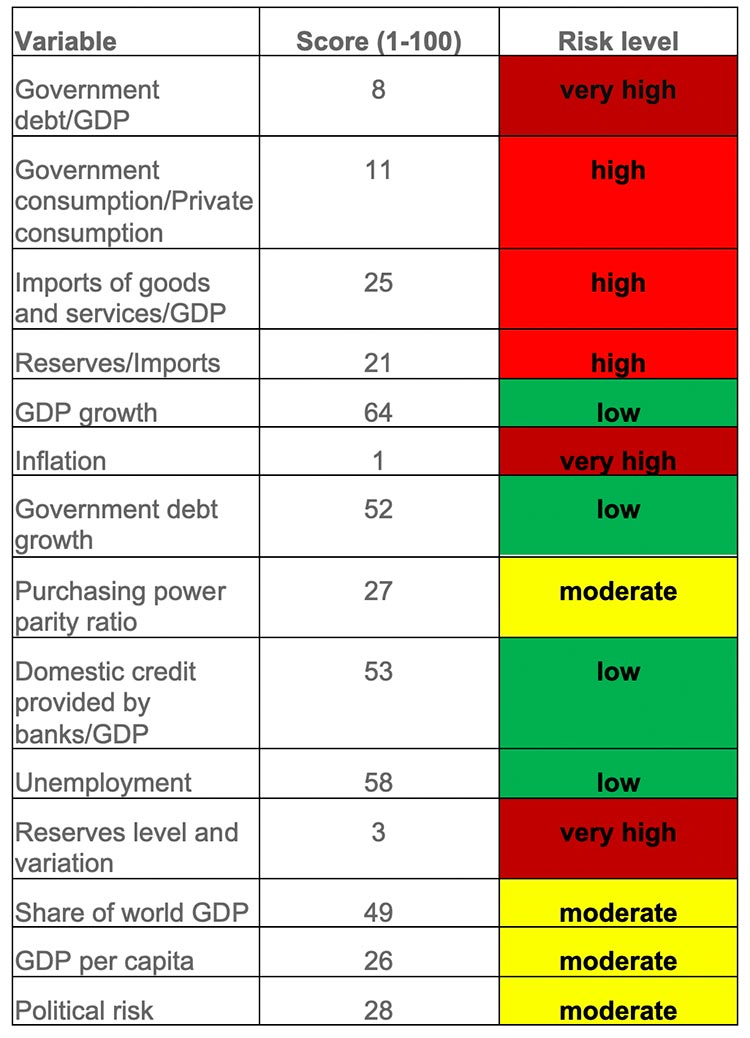

In Table 1, we list the variables used as inputs into StarMine SR, their scores, and a description of how that variable is impacting the model’s output for Sri Lanka.

We coded in dark red, red and yellow the variables that have a score below 11, 26 and 51 respectively.

Variables with a score of 51 and above are marked in green.

According to StarMine SR, the main origins of the Sri Lankan crisis are the high level of government debt per GDP, the large decrease and high variability in reserves, and high inflation and currency devaluation.

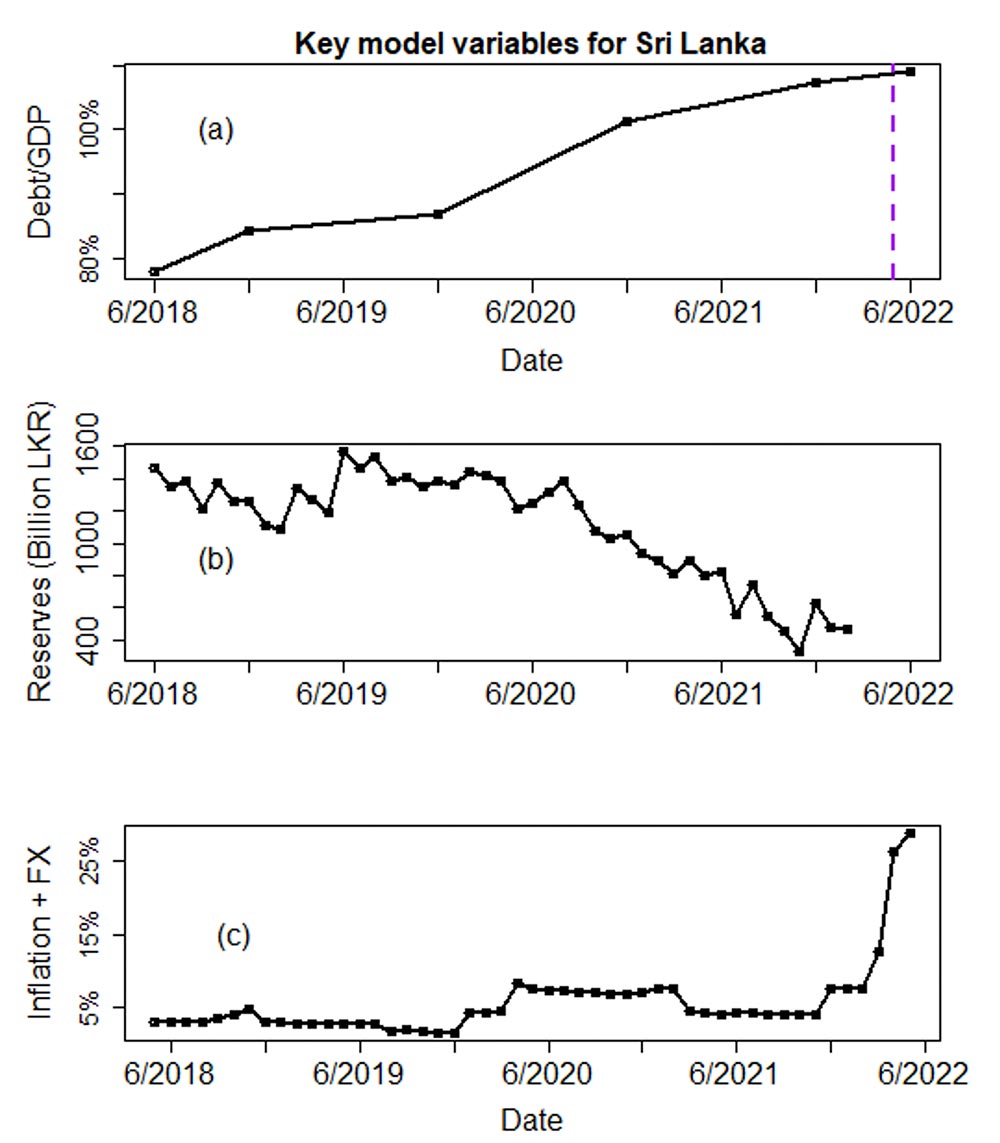

In Figure 2, we plot the values of these variables over time.

Also in Table 1, the following variables are shown to be contributing to the Sri Lankan crisis: government consumption/private consumption, imports of goods and services/GDP, and reserves/Imports.

Table 1. Model variable values for Sri Lanka as of 19/05/2022. Scores vary from 1 to 100, with 1 being the riskiest level.

Figure 2. Sri Lankan government debt over GDP (a), reserves (in billions of LKR) (b), and inflation combined with FX as a function of time (c). The broken line in (a) marks the default date.

Very high risk for a number of years

In summary, StarMine SR had been classifying Sri Lanka as very high risk for several years, culminating with a default in May 2022.

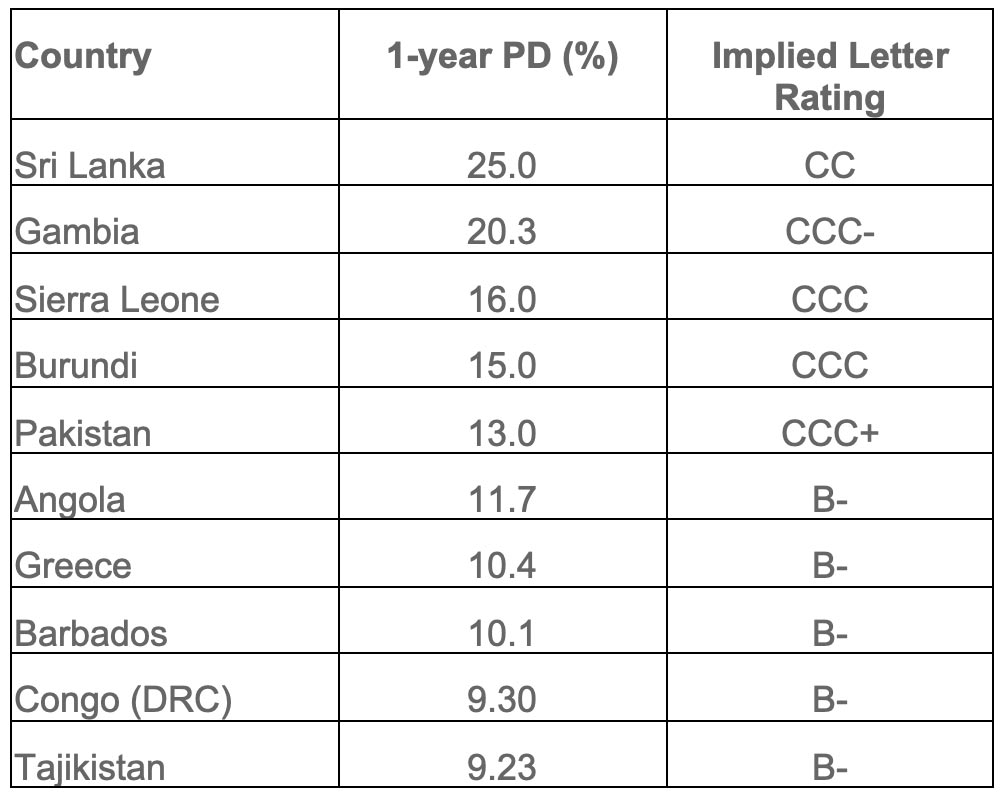

Table 2 displays the ten countries with the highest risk (as of 19/05/2022) as measured by StarMine SR.

Based on this table, the African continent has the most countries in danger of default. Pakistan, Greece and Barbados are the most troubled countries in Asia (when we exclude Sri Lanka), Europe and Latin America, respectively.

Table 2. Top ten countries with highest risk of sovereign default based on StarMine SR as of 19 May 2022

How can Refinitiv help?

Refinitiv’s Economics and Global Macro offering enables finance professionals to create workflow theses faster and with greater accuracy.

Backtest your trading strategies in the CDS and fixed income markets with StarMine SR’s ability to generate a comprehensive picture of sovereign risk. Using a broad spectrum of data points like macroeconomic, market-based and political risk data, it provides robust estimates of sovereign debt defaults over multiple time horizons, so you can make more informed decisions.

Click here to find out more, or to speak to a solution consultant who will demonstrate the capabilities of our Economics and Global Macro offering in-person.