Despite the importance of both global megatrends and Islamic finance to national agendas, there was no thought leadership explicitly linking the two. A report from Refinitiv, in partnership with Islamic Corporation for the Development of the Private Sector (ICD), fills this gap in the market by combining them and analysing them in detail.

- How can Organisation of Islamic Cooperation (OIC) nations apply global megatrends to catalyse their Islamic finance and development agendas?

- The six megatrends highlighted in the report cover technological and societal transformations taking place in OIC countries and the globe.

- OIC nations lag behind the average global digitalisation rate. The report looks at how digital and technological trends could be leveraged to address social transformation.

For more data-driven insights in your Inbox, subscribe to the Refinitiv Perspectives weekly newsletter.

Refinitiv has launched its first-ever Organisation of Islamic Cooperation (OIC) Megatrends Report, for 2022. The report links global megatrends within OIC markets and the world of Islamic finance.

The Organisation of Islamic Cooperation, formerly known as the Organisation of the Islamic Conference, is a federation of 57 sovereign states that are either Muslim majority or have significant Muslim populations.

The report analyses six global megatrends and their impact on the countries that make up the Organisation of Islamic Cooperation, as well as the role Islamic finance plays in unlocking the megatrends’ potential to transform these markets.

For the methodology of the report, the team compiling the findings initially long-listed 100 global megatrends and key drivers before narrowing them down to six global megatrends.

For further insights read: ICD-Refinitiv OIC Megatrends Report 2022

Watch: Islamic Finance Development Report 2021: Advancing Economies

What are the six global megatrends?

The six inter-related megatrends are: Digitalisation, Artificial Intelligence (AI), Transformation, Inequality, Youth, and Ageing Societies.

The first three are technology trends, which are playing out across OIC societies, together with social changes highlighted in the latter three trends. These social trends, in turn, are influenced by technological trends.

Several key insights, including challenges and Islamic finance solutions, emerged for each megatrend.

1. Digitalisation

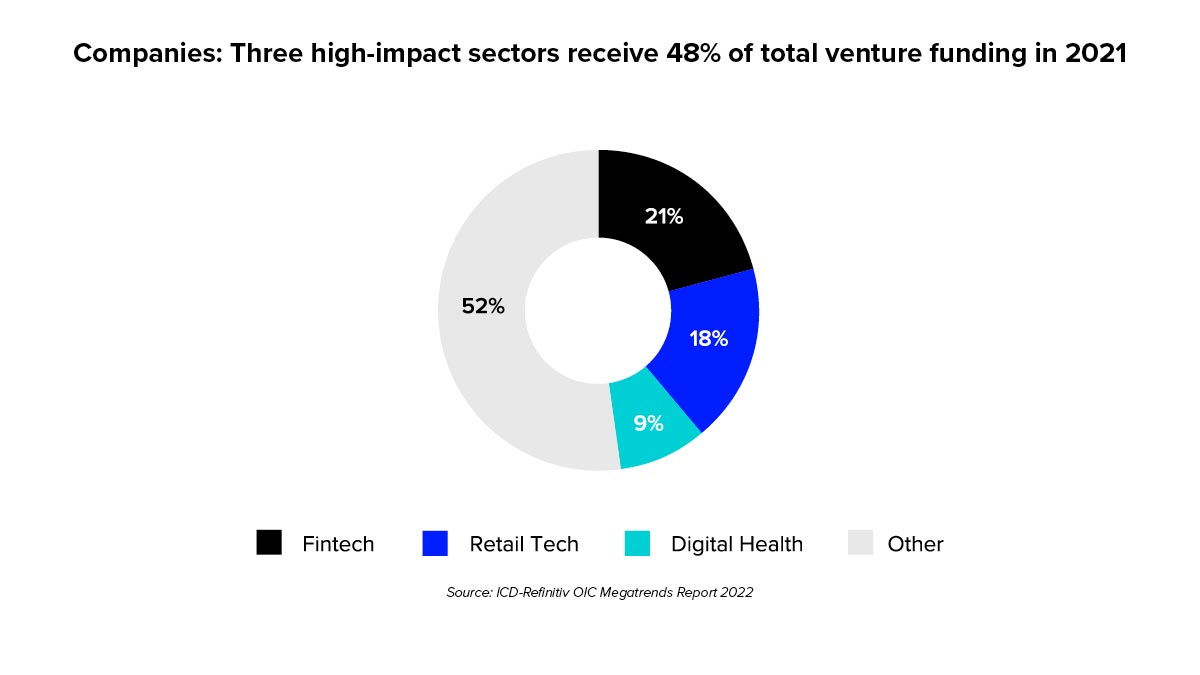

Tech and tech application businesses won high levels of venture capital (VC) funding in 2021 as the COVID-19 pandemic accelerated digitalisation across many sectors.

And while OIC countries also rode the wave, funding remains a key challenge for entrepreneurs and start-ups, signalling the need for more Islamic VC and private equity (PE).

Collectively, the 57 countries within the OIC lag behind the latest developments in digitalisation but some key Islamic finance jurisdictions are developing best-in-class capabilities.

At the same time, dedicated Islamic finance, or Islamic economy enablers such as accelerators, are helping in the drive to enhance OIC entrepreneurial ecosystems.

Only three out of the Top 50 countries in global innovation are OIC nations: UAE, Malaysia and Turkey.

2. Artificial Intelligence

AI is already changing how the world works – but it is still unclear whether it will enhance or restrict human potential.

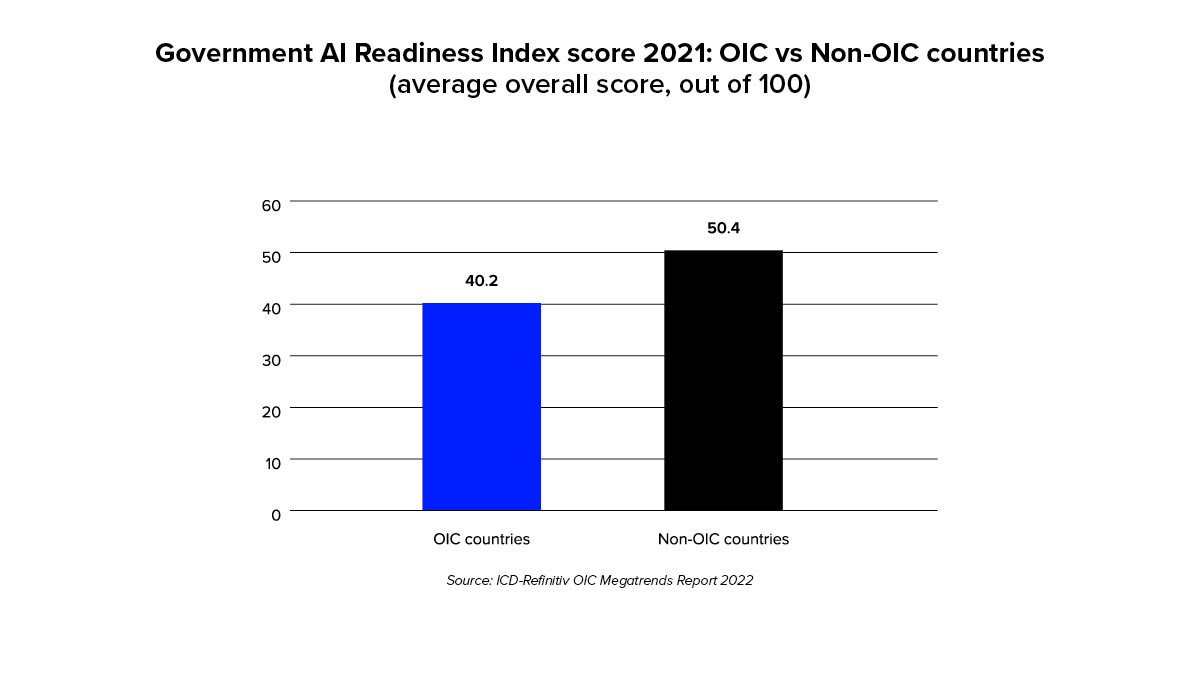

OIC markets vary widely in their readiness for automation and the group as a whole would benefit from more cooperation, especially between leading and late adoption nations.

For OIC governments, AI and automation have deep implications for citizens, while for industry AI-rich platforms provide novel solutions to problems.

More use cases are now emerging from both Islamic banks and Islamic fintechs, resulting in greater customer-centricity and embedded Islamic finance.

The average AI Readiness Index score for OIC countries is just 40.2 out of 100, whereas for non-OIC countries it is 50.4 out of 100.

3. Transformation

Disruption is a key catalyst for sectoral transformations that are now ubiquitous, metamorphosing economies and creating new frontiers for innovation.

Tech-enabled disruptions have also reached Islamic financial services, but more partnerships are needed for them to meet their fullest potential to transform OIC economies.

At the centre of this landscape are Islamic banks, which hold 70 percent of the assets of the global Islamic finance industry. These institutions are not immune to increasing non-financial risks, which calls for a greater need to rethink old economic paradigms.

Challengers such as Islamic digital-only banks and fintechs may, in time, substantially capture demand in OIC countries but, currently, the industry’s ecosystem is still nascent and scale is needed.

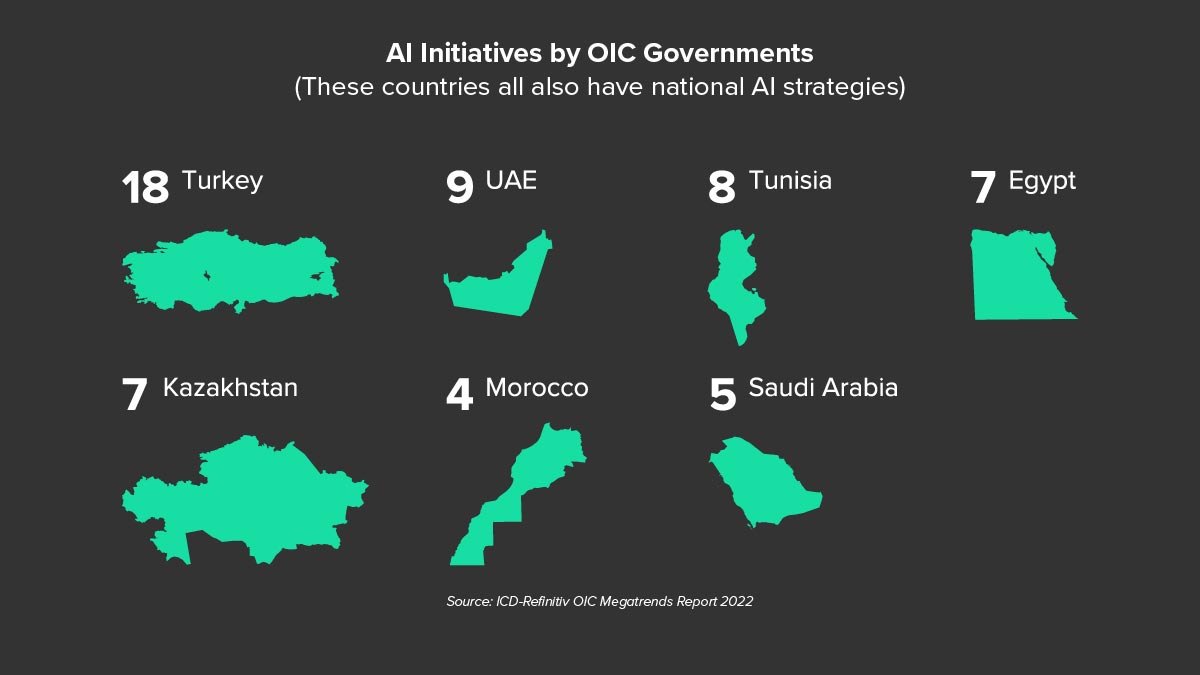

Turkey has 18 AI initiatives and national strategies, the most for any OIC nation.

4. Inequality

Inequality is growing, widening the gap in health and education outcomes globally and thereby entrenching societal problems.

OIC markets are particularly at risk of lower shared prosperity. The top 10 percent have 48 percent of the income distribution across OIC countries; this is slightly better than the global figure of 52 percent.

While redistributive solutions exist in Islamic finance and are slowly reaching critical mass, more funding and awareness is needed.

Several successful organisations actively collect, manage, and disburse funds for Awqaf, and Zakat, and these efforts align with SDG 10.

5. Youth

Younger generations are driving a sea change in consumer preferences and habits. Stakeholders and industry players need to adapt to stay ahead.

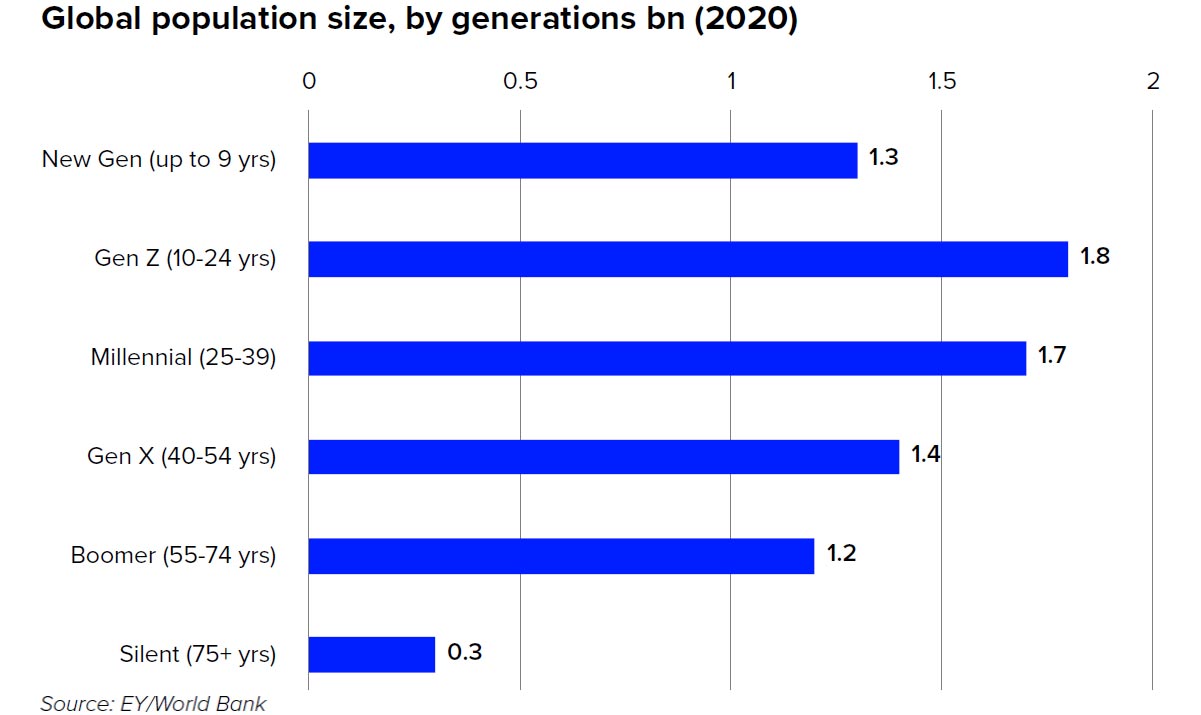

OIC markets are particularly youthful, with a large base of consumers who wish to integrate their faith across their lifecycle needs and identities. According to OIC estimates, member states collectively account for 27 percent of the global youth population, and by 2050 this proportion will increase to 35 percent.

Serving them, Islamic fintechs have started to provide for younger Muslim consumers’ financial lifecycle needs and enable their ambitious aspirations, with several now operating across varying geographies.

In short, ‘localisation’ is one of the keys to wider traction.

6. Ageing Societies

Population ageing is increasing globally – this pushes up old-age support ratios, creating pressure on future workforces and healthcare systems.

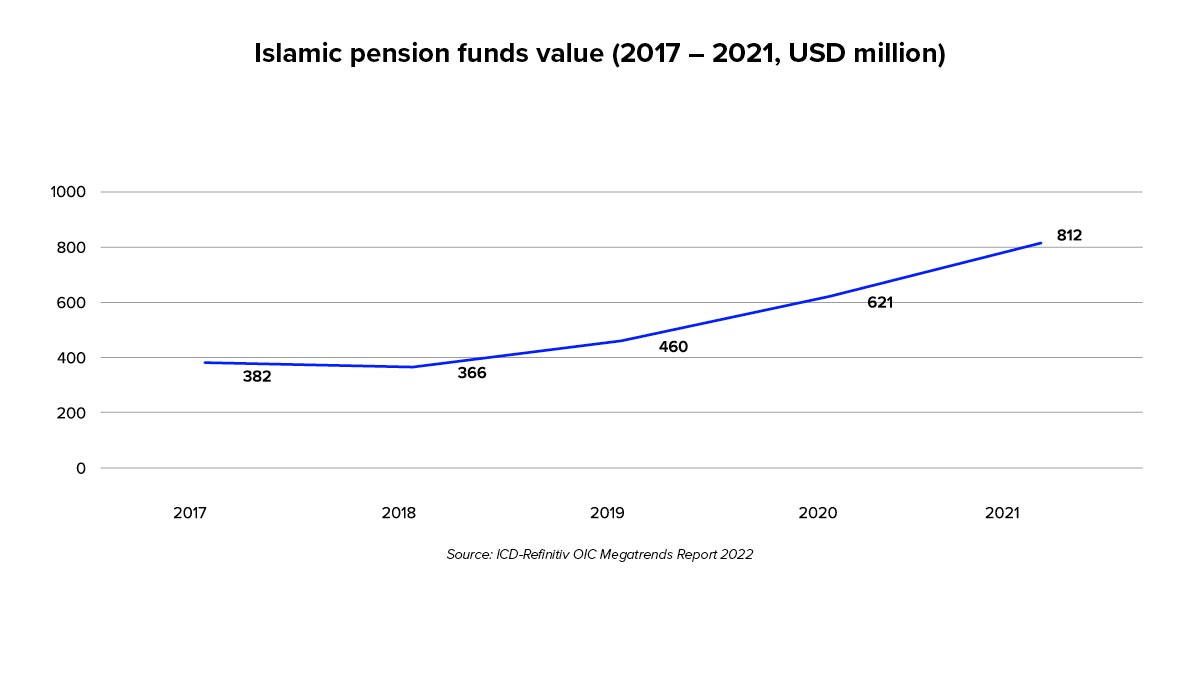

OIC countries are also affected, yet many have limited pension fund resources, indicating citizens are not saving enough for retirement.

Islamic pensions and longevity Sukuk can help reduce retirement savings gaps, but stakeholders need to amplify these solutions.

On a positive note, several Shariah-compliant pension options are already in the market, including occupational pensions and self-driven private retirement schemes.

Meanwhile, Refinitiv data shows that the value of Islamic pension funds is rising. In 2017, their assets were worth $382 million globally by the end of 2021 this number had risen to $812 million.

For further insights read: ICD-Refinitiv OIC Megatrends Report 2022