Covid-19, climate emergencies, war in Ukraine, energy shortages…the global economy has been buffeted by shocks over the last few quarters. But how has this affected the creditworthiness of industries and individual companies?

- As many people required healthcare during the Covid-19 pandemic, the Healthcare sector was the least affected. This was true until around October 2021, when its ratings started to drop again.

- The work from home boom drove the need for more home supplies which benefited the Consumer Non-Cyclical sectors globally.

- Real Estate was the most affected sector, mirroring the change in new ways of working, as many industries moved their people from offices to home.

For more data-driven insights in your Inbox, subscribe to the Refinitiv Perspectives weekly newsletter.

The Refinitiv StarMine Structural Credit Risk (SCR) model helps us answer the creditworthiness question.

Using the Covid-19 outbreak as a case study, we can see that the pandemic caused some sectors traditionally seen as creditworthy to become relatively riskier – and vice versa. And the SCR model tells us that the global economy has still not recovered fully from the disruption caused by lockdowns, supply chain interruptions and inflation.

What is the StarMine Structural Credit Risk model?

The SCR approach is based on an improved version of a model originally developed by Robert Merton in 1974, which models a company’s equity as a call option on its assets. The SCR covers over 45,000 global securities.

The SCR has been shown to predict 85 percent of default events within a 12-month horizon in its bottom quintile of scored companies.

Based on a past study, the SCR performed better than the popular Altman Z-Score approach to modelling credit risk. Another study showed the SCR can predict the direction of changes in credit default swap (CDS) spreads.

The default probabilities calculated by the SCR model are mapped to letter ratings (as in a traditional credit rating system) and also ranked to create 1-100 percentile scores.

What happened during the pandemic?

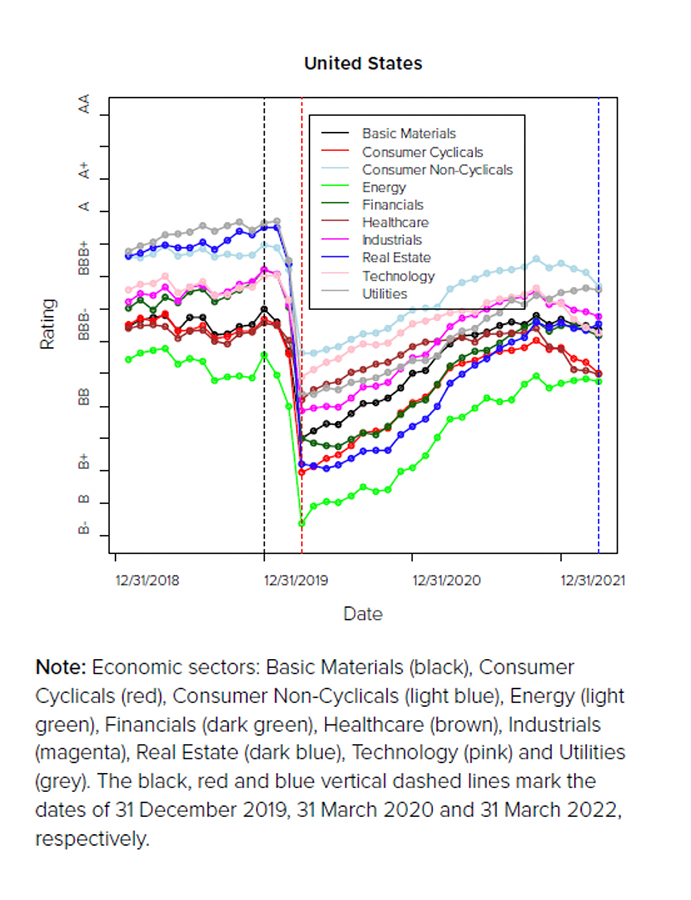

A chart of the SCR letter ratings for US company sectors shows the dramatic fall in credit scores in early 2020 as Covid-19 impacted economic activity.

Figure 1: Letter rating evolution for different economic sectors in the United States

Against this overall trend, some sectors did better than others from a credit risk perspective.

For example, Real Estate was the US sector with the second-highest quality rating in the run-up to the pandemic. But it then plummeted to second-bottom as investors worried about the potential economic impact of the new work-from-home culture – vacant offices, falling rents and declining capital values.

But two other sectors (Consumer Non-Cyclical and Technology) prospered from the same post-coronavirus shift: the internet enabled people in a variety of jobs to work easily from home, while technology-based services made it possible for many companies to adapt. And to work from home, people needed more supplies, which benefited Consumer Non-Cyclical companies.

What about the recovery from the pandemic? The upwards-sloping coloured lines in the right of Figure 1 tell us that there’s been a general improvement in creditworthiness since early 2020.

But no sector has regained its pre-Covid letter rating. Other factors, such as the emergence of new coronavirus variants and disruptions to global supply chains, have dampened the economic recovery.

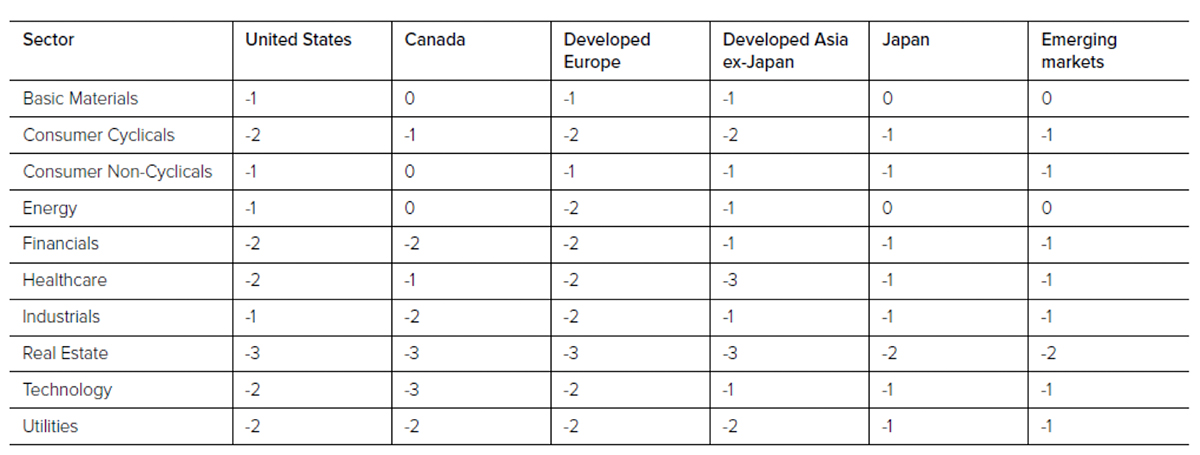

These US sector shifts were largely replicated in the SCR model scores for Canada, Developed Europe, Developed Asia ex-Japan, Japan and Emerging Markets. Unsurprisingly, in most regions, Real Estate shifted from being one of the least risky to one of the riskiest sectors (although this trend was less evident in Emerging Markets).

Another result was that Developed Asia ex-Japan, Developed Europe and Emerging Markets had smaller variations in credit scores (from end 2019 to March 2022) when compared to the United States, Canada and Japan.

Which sectors recovered most and least?

Figure 2 shows how the SCR model assessed the change in creditworthiness of different sectors across different countries and geographic regions. The change is calculated from immediately pre-pandemic (December 2019) to March 2022. The change is expressed in terms of implied credit rating ‘notches’.

Figure 2: Variation in credit rating ‘notches’ for different economic sectors in different countries/regions between 31 December 2019 and 31 March 2022

It’s clear that Real Estate has suffered the largest credit impairment over the period, suffering a decline of two or three notches across regions. Other sectors, such as Basic Materials, Consumer Non-Cyclicals and Energy, have seen a relatively smaller drop – or no change at all in some regions.

Although the latter three sectors are the closest to achieving pre-pandemic levels, no sector in any country or region has surpassed the rating that it had at the end of 2019.

Meeting investors’ needs

The Refinitiv StarMine SCR model offers a sensitive and forward-looking view of corporate creditworthiness.

With the world economy continuing to suffer major disruptions, the SCR meets investors’ needs for innovative solutions that meet the rising challenges of managing and moderating credit risk.

Want to know more?

This report highlights some of the key findings from a recent StarMine white paper, that uses the Refinitiv StarMine Structural Credit Risk model to analyse the changes in the credit of different economic sectors for different countries, during the Covid-19 pandemic.

Read the StarMine white paper: Exploring the Impact of Covid-19 on Corporate Credit