We explore the findings of the 2022 Islamic Finance Development Indicator (IFDI), which provides an overview of the industry by measuring the state of the development of Islamic finance in 2021, and presents sub-sector performances and rankings for 136 countries around the world.

- The total global net income reported by Islamic financial institutions in 2021 trebled from US$10.5bn in 2020 to US$32.0bn in 2021, signalling improved outcomes, especially for Islamic banks.

- The enhanced Islamic Finance Development Indicator incorporates Islamic fintech and sustainability, and gives more weight to financial performance and governance components. Malaysia, Saudi Arabia and Indonesia top the IFDI 2022.

- The report based on the IFDI findings is launched in partnership with the Islamic Corporation for the Development of Private Sector (ICD) of the Islamic Development Bank Group.

For more data-driven insights in your Inbox, subscribe to the Refinitiv Perspectives weekly newsletter.

Following a difficult 2020, economies started to get back on track in 2021.

However, even as many countries began to re-open their economies, they were hit by new waves of COVID-19 that stalled their momentum and led to fresh lockdown or safety measures, which again disrupted global supply chains and increased the cost of transport.

However, 2021 ended on a better note as high vaccination rates prompted most countries to loosen their pandemic-related restrictions.

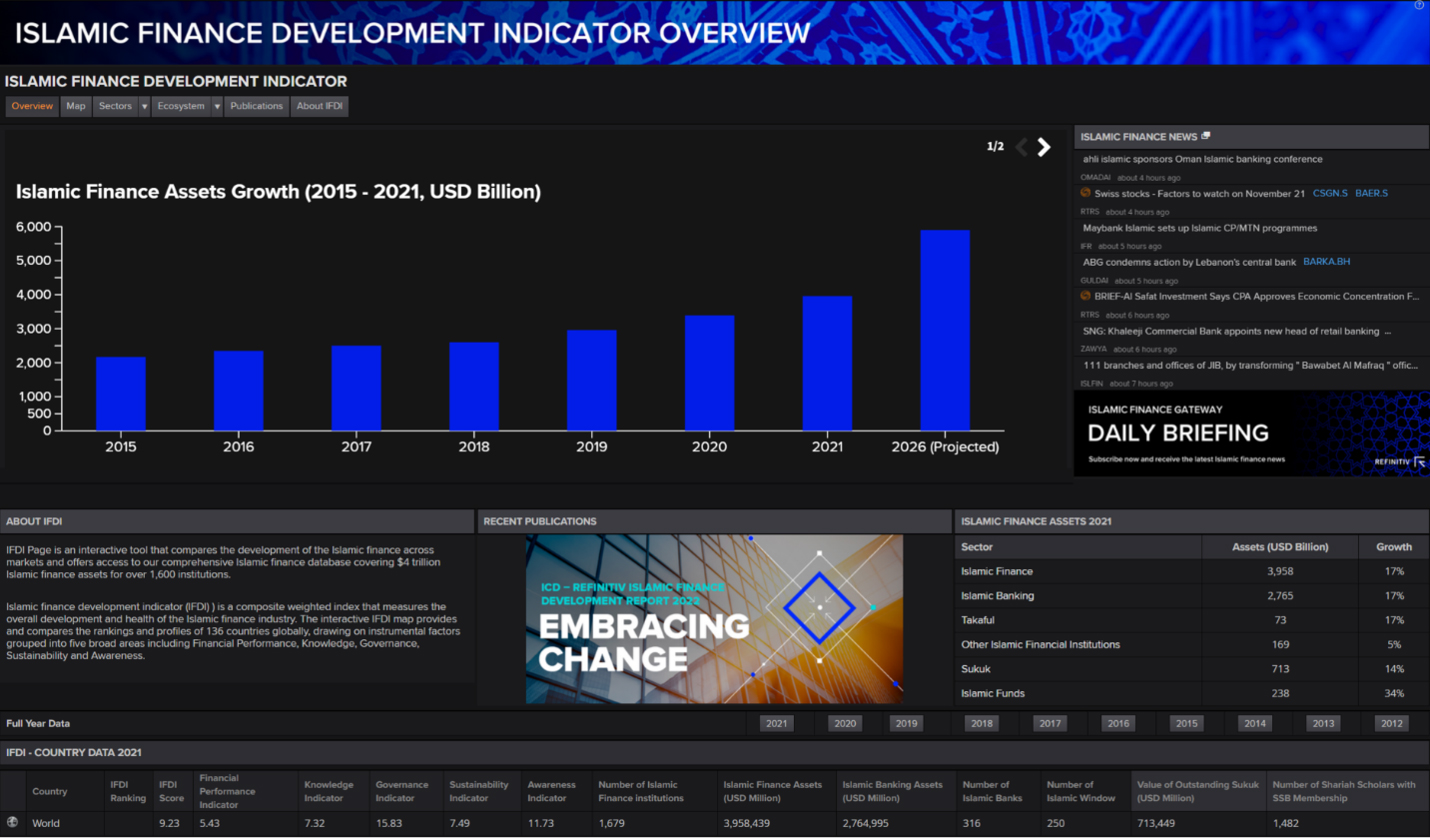

In 2021, Islamic finance industry reached almost US$4.0trn in total assets, which represented growth of 17 percent – up from 14 percent in 2020 – according to the Islamic Finance Development Report 2022.

The top countries ranked by Islamic finance assets are Iran, Saudi Arabia and Malaysia. Among the counties with the biggest rise in assets are Russia, Canada, the United States, Maldives, Nigeria and Tajikistan.

The growth in these countries is mainly attributed to Islamic funds, sukuk and Islamic banking.

Read the Islamic Finance Development Report 2022: Embracing Change

Islamic banking rebounds

By sector, Islamic banking is the largest sector in the Islamic finance industry, holding 70 percent of its assets or US$ 2.8trn in 2021, a 17 percent increase on 2020.

in 2021, the sector breathed a sigh of relief as provisions for credit losses eased, pushing up net income substantially. Eighty-nine percent of Islamic banks or conventional banks with Islamic banking windows reported a net profit.

In addition, 72 percent of such banks reported positive performance as indicated by a rise in net profit when compared with 2020 or a decline in net loss.

There were three key underlying growth drivers: in some instances, Islamic banks benefited from extended government support to sectors that were pandemic-hit; a small number gained operational efficiencies from moves such as branchless banking and partnering with fintechs; and there was a continued high demand for Islamic banking in different countries.

Islamic capital markets are thriving

Sukuk, the second largest sector by assets, grew by 14 percent in 2021 to US$713bn in sukuk outstanding. New issuance rose by 9 percent to a record US$202.1bn.

Notably, long-term sukuk with tenors of five years or longer increased, indicating a shift in perspective towards the horizon post-pandemic. Sovereigns and quasi-sovereigns continued to dominate new issuances. They also continue to dominate in the issuance of ESG sukuk that in 2021 reached a new high of US$5.3bn.

Saudi Arabia, Indonesia and Malaysia are the clear leaders in sukuk and we anticipate that sukuk will continue to grow, especially with the ESG investments becoming mainstream and strong Gulf Cooperation Council (GCC) demand helping fund green and sustainability transition projects.

Non-core markets such as Bangladesh and Egypt also contributed towards sukuk growth.

Islamic funds, the third biggest sector, saw impressive growth of 34 percent to US$238bn worth of assets under management in 2021. However, this sector is less widespread than banking and sukuk, with a substantial 81 percent of total global Islamic funds coming out of just three countries: Iran, Saudi Arabia and Malaysia.

Money market and equity mutual funds were the biggest asset classes, but it is the exchange traded funds (ETFs) that gained traction, with more appearing in different countries such as Canada, Russia and Australia.

As with sukuk, ESG funds hit a landmark in the development of Islamic finance in 2021.

One of the highlights was the announcement by Malaysia’s Employee Provident Fund (EPF) – which holds substantial Islamic funds – of its transition to be a sustainable investor with a fully ESG-compliant portfolio by 2030 and climate neutral portfolio by 2050.

New indices that could shape the sector in some countries such as Saudi Arabia were welcomed and it is about to see the entrance of potentially significant players backed by large Islamic banks.

How are non-banking financial institutions faring?

Other Islamic financial institutions (OIFIs) – including financial technology companies, investment firms, financing companies, leasing and microfinance firms, and brokers and traders – grew by 5 percent to US$169bn worth of assets.

Some of the fastest growth in assets was recorded in Kazakhstan, Egypt and Maldives.

A headline segment in this sector is financial technology, or fintech, which is a key focus for Saudi Arabia that has plans to almost triple its number of fintech firms from 82 to 230 by 2025.

Takaful is the smallest sector of the Islamic finance industry, holding US$73bn in 2021 on the back of a strong 17 percent growth.

The sector is undergoing consolidation in the GCC countries that will streamline and reduce costs. This is especially important because it is facing increased competition from its conventional counterpart. Meanwhile, big regulatory changes in Southeast Asia will strengthen governance in Indonesia and Malaysia, as well as potentially welcome new entrants in the Philippines and Tajikistan.

Introducing the enhanced IFDI model

The growth of the asset sizes of the five sectors of Islamic finance – Islamic banking, sukuk, Islamic funds, other Islamic financial institutions and takaful – contribute to the financial performance of the Islamic Finance Development Indicator (IFDI).

As a barometer of the whole industry, the IFDI also factors in key aspects of the ecosystem: Governance, sustainability, knowledge and awareness.

Apart from this, we have made three key changes to enhance the IFDI model:

- The addition of new metrics related to ESG and Islamic fintech;

- A re-arrangement of some of the previous metrics to form new sub-indicators;

- A change of the weightage of the five main indicators by stressing more on the financial components (40 percent from 20 percent) and governance (25 percent from 20 percent), while the remaining weightage is distributed among the remainder of indicators.

For IFDI 2022, the core Islamic finance markets in Southeast Asia, the GCC and South Asia lead the 136 countries we assessed.

The IFDI added the new metric of FinTech Sandbox to the governance indicator this year, keeping in step with industry developments.

Regulations are the backbone of Islamic finance governance, with Islamic banking being the most widely covered in different countries. Shariah governance is the second strongest after regulations, as several countries have centralised Shariah boards and most have Shariah scholars who represent Islamic financial institutions.

Corporate governance is the weakest, as many financial institutions returned weak reporting scores. Malaysia, Oman, Bahrain, Pakistan and Kuwait are the leaders in governance.

On the sustainability indicator, the IFDI considers CSR funds disbursed and ESG practices for all Islamic finance sectors and asset classes. This is one key indicator to watch as the world’s financial industry overall continues to improve on ESG practices.

For the Islamic finance industry, Malaysia, Saudi Arabia, Singapore, South Africa and Jordan are the top countries.

On the knowledge indicator, Indonesia overtakes Malaysia to rank first with its widespread efforts on both education and research. After Malaysia in second comes Saudi Arabia, Pakistan and Bahrain.

Meanwhile, the awareness indicator measures the number of Islamic finance events and news. Malaysia is top-ranked, followed by the GCC countries Kuwait, Saudi Arabia, UAE and Bahrain.

Future large-scale growth drivers

At the time of writing, moving into the fourth quarter of 2022, economies are hit by the continuing Russian invasion of Ukraine that is affecting energy prices and sending ripples through a large cross-section of the world’s supply chain. Inflation is also a major concern for most countries.

Looking specifically at Islamic finance, several large-scale national plans and roadmaps will give the industry a boost. These include initiatives in Afghanistan, Brunei, Indonesia, Kazakhstan, Labuan, Malaysia, Oman, Pakistan and Saudi Arabia.

Key developments across North Africa where Islamic banking and takaful are gaining a lot of traction and growth, will also contribute to the expansion of Islamic finance moving forward.

The other region to look out for is Central Asia where countries like Tajikistan, one of the fastest growing Islamic banking markets in 2021, will also kickstart its takaful sector. Kazakhstan is also fast expanding its Islamic finance industry with strong growth in Other Islamic Financial Institutions, especially FinTechs.

Overall, IFDI projects the global Islamic finance industry to grow to US$5.9trn by 2026 from US$4.0trn in 2021, mainly driven by its biggest segments Islamic banking and sukuk.

Get the IFDI raw data on Eikon/Workspace

Eikon/Workspace users can access the underlying data for the Islamic Finance Development Indicator app.

The database is comprehensive and can be downloaded in Excel sheet format with the details of every Islamic institution that discloses its financials with a dollar-by-dollar breakdown of the industry.

The data includes over 1,600 Islamic financial institutions including Islamic banks and takaful operators along with sukuk, Islamic funds and Shariah scholar for different countries around the globe. This includes the newly introduced metrics for IFDI such as ESG sukuk and Islamic funds along with Islamic fintechs.

Read the Islamic Finance Development Report 2022: Embracing Change