Richard Segarra, analyses the effectiveness of StarMine models and the added value of factor investing in equity markets from 2021-2022, in two different market environments.

- In long-only and market-neutral applications most StarMine models beat the market and their benchmark in two quite different market environments across multiple regions.

- StarMine models proved useful when applied in a market-neutral strategy, as evidenced by every StarMine model having positive top-bottom decile spreads and which were mostly more effective than benchmark models.

- For 2021, except for Intrinsic Valuation, every model had a positive top-bottom decile spread exceeding its benchmark. For Q1 2022, eight of the eleven models presented continued to show added value compared to benchmarks.

For more data-driven insights in your Inbox, subscribe to the Refinitiv Perspectives weekly newsletter.

After the outstanding returns in 2021, equity markets slumped in the first quarter of 2022.

With the change in direction of the equity markets, investors are wondering whether the factors that worked during the market advance remain effective.

Equity outperformance

Insights on where equity outperformance were achieved are found by comparing the performance of various well-designed factor models within long-only and market neutral applications.

In this case, we examine the effectiveness of the StarMine models in these two different market environments.

In the strong overall market of 2021, the benefit of factor investing was clear. Value factors were particularly good, but models that combined multiple factors also did very well.

StarMine models not only matched this general trend, but in nearly all cases, provided added value over comparable benchmark models.

With the decline in Q1, the performance of factor selection held up on a relative basis and StarMine continued to compare favourably across model offerings.

StarMine models’ performance

The graphs above depict each StarMine model’s top decile average return compared to equal-weighted average return of all stocks.

This would be comparable to a long-only strategy.

- Except for Insider Filings, all StarMine models produced top decile performance that exceeded the equally-weighted average return of the overall universe of stocks in 2021.

- Combination models, Analyst Revision Model (ARM) and the value models Relative Valuation (RV) and Intrinsic Valuation (IV) had top decile returns that beat the market average by an impressive margin.

- The better performance of Value Momentum (Val-Mo) compared with the Combined Alpha Model can be attributed to the fact that the Combined Alpha Model includes additional factors to those common with Value Momentum that, while still positive, had relatively lower top decile returns.

- Although the market turned lower in Q1, the trend of outperformance of StarMine models held up.

- Only Insider Filings and MarketPsych Media Sentiment (MMS) had below market average top decile returns. Notably, Relative Valuation and Value Momentum were able to produce positive top decile average returns.

- Value Momentum’s top decile average return was also higher than the top decile average returns of any of its constituent models.

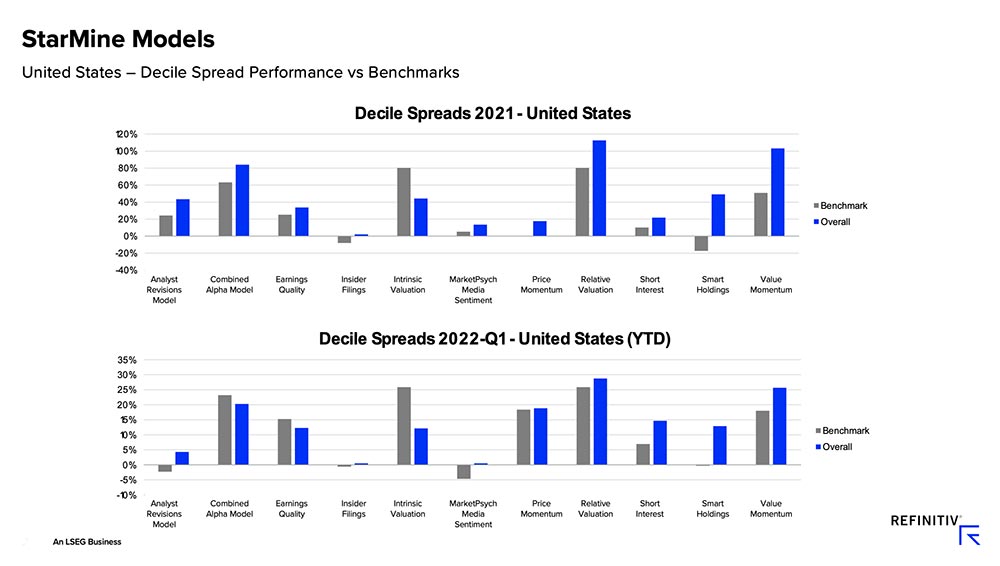

Market neutral strategy

StarMine models also proved useful when applied in a market-neutral strategy.

- The top-bottom decile return spreads for each StarMine model is compared with that of its corresponding benchmark model.

- Every StarMine model had positive top-bottom decile spreads and were mostly more effective than benchmark models.

- For 2021, except for Intrinsic Valuation, every model had a positive top-bottom decile spread exceeding its benchmark. For Q1 2022, eight of the eleven models presented continued to show added value compared with benchmarks. Combined Alpha Model, Intrinsic Valuation and Earnings Quality (EQ) were the exceptions.

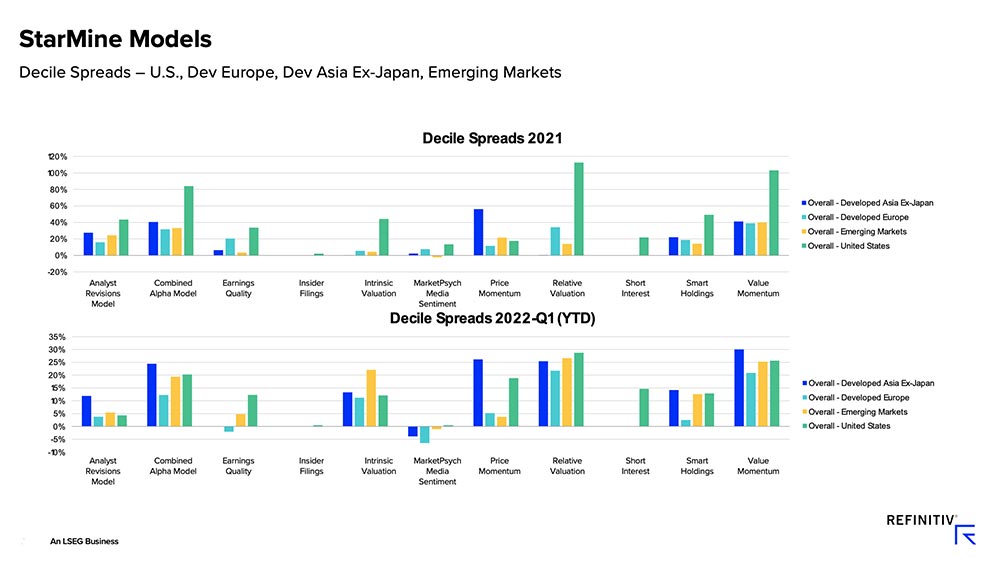

Global performance

The effectiveness of StarMine models was evident globally as shown in the top-bottom decile spread of average returns for each model regionally.

- For 2021, StarMine models successfully predicted better and worse performers in each region. With few exceptions, Combination models were more discriminating than classic factors or smart money models across regions. The exceptions were Price Momentum (PriceMo) in Developed Asia-ex Japan and Relative Valuation in Developed Europe (vs. Combined Alpha Model only) and United States.

- Notably, in Q1 2022 value factors as represented within Relative Valuation showed strong top-bottom decile spreads across regions. For Developed Asia ex-Japan, the strong decile spread for Price Momentum and Relative Valuation contributed to a superior decile spread for Value Momentum in that region in Q1 2022.

- In terms of the relative performance of combination models, what held for the U.S. was also true in other regions.

- Combined Alpha Model’s inclusion of additional models to Value Momentum that had relatively lower decile spreads diluted the benefit of the inclusion of Price Momentum and Relative Valuation in Q1.

Highly effective models

Examining these results over 2021 and Q1 2022 we see that StarMine models have proven to be highly effective. In long-only and market-neutral applications, most StarMine models beat the market and their benchmark in two quite different market environments across multiple regions.

The universes presented include the top 3,000 in the United States, 1,000 in Developed Asia-ex Japan, 2,000 in Developed Europe, and 1,500 in Emerging Markets, and they exclude micro-cap stocks. Performance results reflect monthly rebalancing and exclude transaction costs.

The service does not constitute a recommendation to buy or sell securities of any kind and Refinitiv has not undertaken any liability or obligation relating to the purchase or sale of any securities for or by you. Performance data quoted represents past performance and does not guarantee future results.