U.S. financial conditions have eased almost 100 bps in the past month, according to Goldman’s FCI. This is not what the Fed wants to see, because – as Bostic and Waller have indicated – it puts the Fed in a bind. Reuters columnist Jamie McGeever looks at what may come next.

- The euphoria that engulfed markets last week after surprisingly soft U.S. inflation figures was understandable.

- But be careful what you wish for. The surge in stocks and bonds, and steep dollar slide last week sparked one of the biggest loosening of financial conditions in decades.

- If that continues, the Fed may feel obliged to step even harder on the rate-hiking pedal – cutting across markets just like it did this summer.

For more data-driven insights in your Inbox, subscribe to the Refinitiv Perspectives weekly newsletter.

The opinions expressed here are those of the author, a columnist for Reuters.

What ensues is a risky cat-and-mouse game. Even if the Fed thinks inflation is on the wane and its policies are gaining traction, a premature easing of market-driven financial conditions that are based on that very assumption can undermine the central bank’s battle.

Even if the Fed delivers the remaining tightening now expected a sharp drop in borrowing costs across the economy – in loan, mortgage, or credit card rates – or a surge in stock prices could end up sustaining demand, buoying inflation and making the Fed’s job harder.

Fed Governor Christopher Waller fired a warning shot on 13 November, reminding investors that the October inflation report was “only one data point”. More of his colleagues may need to sing from his hymn sheet if they want to avoid finding themselves in a policy pickle soon.

“Easier financial conditions risk undoing the Fed’s work to bring inflation sustainably down to target,” Goldman Sachs’ currency strategy team wrote on 14 November. “We see this as another example of the inherent challenges that come from trying to slow the pace of hikes without easing financial conditions.”

Reuters News: Authoritative, market-moving and objective. News you can trust.

Self-fulfilling prophecy

It’s a tricky juggling act – tightening policy enough to get inflation firmly back down towards the 2 percent target, steering the economy to a ‘soft landing’, and hoping markets keep their feet on the ground to avoid the need to tighten again.

Some real economy measures of financial conditions are tightening. Average mortgage rates have doubled in the last year to more than 7 percent, and the Fed’s Senior Loan Officer Survey shows lending standards to firms at levels typically consistent with recession.

But the easing of financial conditions on 10 November via moves across a range of markets was nothing short of historic, according to Goldman’s U.S. Financial Conditions Index (FCI).

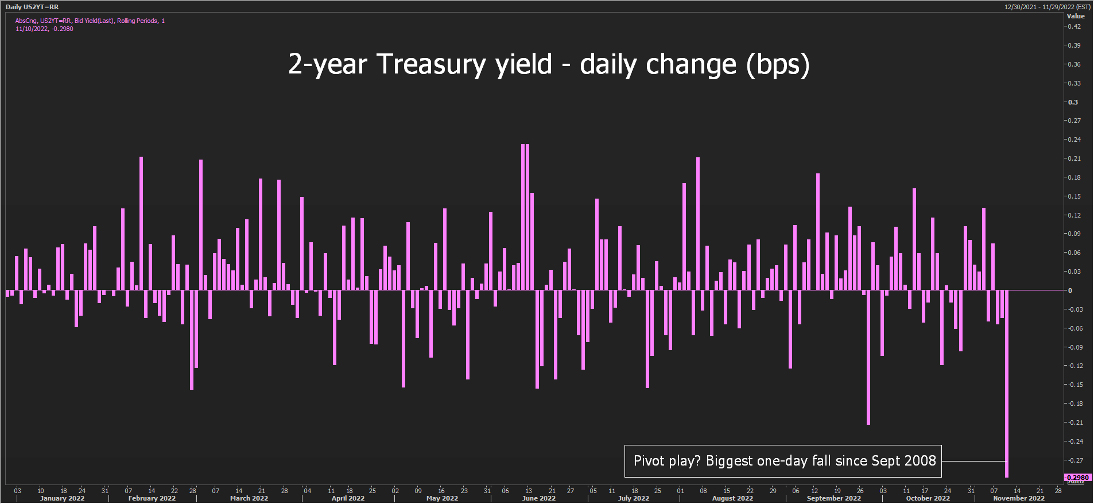

The index posted the third-biggest fall since its launch in January 1990, falling to 100.21 from 100.70 the day before, as Wall Street and Treasuries rallied, and the dollar plunged.

This effectively signalled 50 basis points of easing in a single day, on par with major policy announcements in the Great Financial Crisis and COVID crisis.

Zoom out a little, and the FCI’s decline in recent weeks has now unwound the nearly 80 bps of tightening since the Fed’s September 20-21 meeting, when policymakers issued more hawkish ‘dot plot’ forecasts of where they see policy rates headed.

Every time investors and traders begin to price a Fed ‘pivot’, market conditions loosen, and inflationary pressures rise.

“Easing financial conditions make the Fed’s job of bringing down inflation harder, which in turn actually makes a pivot less rather than more likely. So, the opposite of a self-fulfilling prophecy,” Deutsche Bank’s Jim Reid said on 14 November.

Cumulative effect

Any sense of accomplishment Fed officials might have felt has likely evaporated and now been replaced with trepidation.

Fed Vice Chair Lael Brainard on 14 November struck a slightly more dovish tone than Waller, and it will be fascinating to see which of the two camps investors put more store in.

Broad measures of financial conditions play a central role in shaping the Federal Open Market Committee’s thinking. Chair Jerome Powell said as much after the fourth consecutive 75 bps rate hike in September.

Policy decisions affect financial conditions immediately, but the full effects of changing financial conditions on inflation are felt much later, Powell told reporters. These long lags are “challenging,” he said.

“So we are very much mindful of that. And that’s why… at some point, as the stance of policy tightens further, it will become appropriate to slow the pace of rate hikes while we assess how our cumulative policy adjustments are affecting the economy and inflation,” he said.

History shows that when the Fed reaches its terminal rate – currently priced around 4.90 percent for the middle of next year – the first rate cut of the next easing cycle usually comes within months.

The main outlier in the past 50 years is the June 2006-September 2007 hiatus of 16 months between the final rate hike and first cut of the new cycle. May 2000-January 2001 and December 2018-July 2019 were both eight-month gaps between the final hike and first cut.

Every other ‘pivot pause’ over the past half-century, however, has been much shorter – five months in 1995, and no more than three months in the several episodes scattered throughout the 1970s and 1980s.

U.S. rates futures markets are currently penciling in around 50 bps of easing in the second half of next year.