Refinitiv’s 2022 carbon survey emphasises the importance of carbon markets in reducing greenhouse gas emissions, while respondents expect prices to rise significantly in almost all carbon markets through 2023, and also anticipate strong growth for the voluntary carbon market.

- Carbon markets are seen as more important than ever to reduce greenhouse gas emissions. Our 17th annual carbon market survey finds that stricter carbon constraints are causing companies to cut their emissions.

- Survey respondents expect prices to rise significantly in almost all carbon markets, from North America to China to Europe. A majority of respondents see European carbon prices rising to €100 this year or in 2023.

- Our findings reflect strong growth expectations for the voluntary carbon market (VCM). From a record year in 2021, more than two-thirds of respondents assume even higher activity during this year and next.

For more data-driven insights in your Inbox, subscribe to the Refinitiv Perspectives weekly newsletter.

Greenhouse gas emission trading systems are causing firms to cut carbon. Even with other factors like high energy prices in play, our survey respondents see Europe’s carbon market as a major incentive to cut their CO2 output. Correspondingly, they expect prices for emission permits to rise significantly.

Markets matter

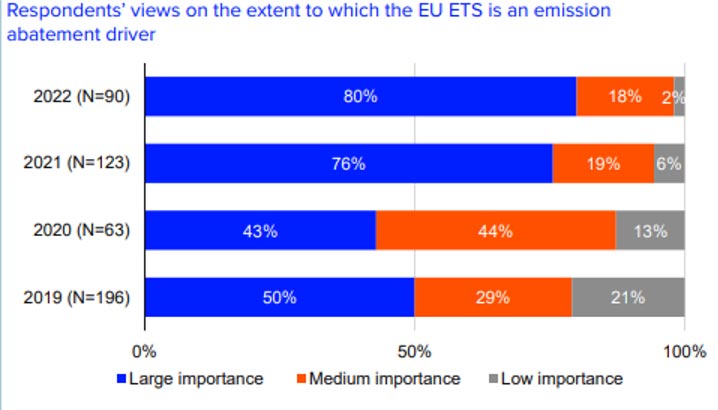

Participants in our annual carbon market survey think the EU’s emissions trading system (ETS) influences companies’ greenhouse gas reduction more than other factors like renewables and energy efficiency policies or high energy prices.

For the second year in a row, a record share of respondents say the EU ETS plays a role in emission reductions. This is particularly significant given the skyrocketing prices of energy products caused by the Ukraine war.

Our survey was taken well after the Russian invasion had started and global energy prices were rising, but respondents still cited Europe’s flagship greenhouse gas policy as overwhelmingly influential to carbon reduction.

The importance of the EU ETS as an emission reducer is now at an all-time high in the nearly two-decade history of our survey. In this year’s survey, 98 percent say the carbon market carries “large importance” in affecting European emitters’ greenhouse gas output.

The ETS incentivises firms to emit less carbon by making the right to do so an increasingly scarce commodity.

Regulators set a limit on the total amount of emissions European power plants and industrial facilities may add to the atmosphere in a year – and requires them to buy permits (European Union Allowances or EUAs) to do so.

The limit decreases over time, so the total emissions from all the covered entities decreases – but firms are able to choose whichever way of cutting carbon works best for them.

In operation since 2005, the EU ETS is now undergoing a major overhaul in line with the EU’s Fit for 55 plan. Regulators are haggling over how to tweak it enough to achieve Europe’s overall goal to reduce greenhouse gas emissions by at least 55 percent by 2030.

It’s therefore no wonder that survey respondents think Europe’s carbon market is a big driver. The price increases they expect in the near future are higher than ever.

Given that achieving the 2030 climate target will require a major tightening of EUA supply, carbon market participants think their price will shoot up.

A majority of respondents see prices for the EU market’s benchmark contract (an EUA for delivery in December) rising to €100 this year or in 2023. They currently range from €80-€90.

The war in Ukraine plays a role here, both directly in terms of raising prices for energy products and indirectly in terms of forcing leaders to turn Europe’s economy away from fossil fuels even faster.

Independence from Russian fossil fuels is now a top priority, strengthening the call for energy efficiency, accelerated build-out of renewable energy, and faster reduction of greenhouse gas emissions. See our previous blog on how the Ukraine war could accelerate the implementation of a more sustainable energy policy in Europe.

Not just Europe: carbon pricing on the rise

These bullish expectations aren’t confined to the EU ETS. Survey respondents following other major carbon markets, such as North America’s Western Climate Initiative (WCI) and the Regional Greenhouse Gas Initiative (RGGI), expect significant price increases for emission permits, too.

While the benchmark contract for an allowance in the WCI ranged from $14-$18 (~€12-16) during 2017-2020, the past year has seen the WCI’s benchmark contract price average $25-$35 (~€21-30).

Indeed, the two North American programmes are undergoing revamps as well. The WCI’s biggest participating jurisdiction is California, which is trying to cut its emissions by 80 percent from their 1990 levels by 2050.

Unlike its east coast counterpart RGGI, which covers only power plants, the WCI covers the transport sector as well. This affects petrol prices, which are already higher in California than most of the U.S.

Respondents were also bullish about prices in China’s national ETS, which began seeing actual transactions in July 2021.

Though the weighted average price for an emission allowance in that programme was about 44 CNY/tonne (~€6) in 2021, those who answered price questions on our survey see the average 2022 price ranging from 50-70 CNY.

Chinese carbon market watchers are also bullish about additional sectors being included. Although the Chinese ETS currently covers only the power sector, the intent of the programme has always been to include a larger share of China’s economy, with more sectors being added over time.

Asked which sectors will be next, respondents chose iron and steel production most frequently – both last year and in this year’s survey.

The expectation of metals being covered next also reflects Chinese concerns about the EU’s carbon border adjustment measure (CBAM), which is set to impose a levy on imports of carbon-intensive products to the extent that the cost of emissions associated with their manufacture is not reflected in their price.

China is one of the world’s largest exporters of iron and steel, and Europe could start applying the CBAM in the next few years. If iron and steel are covered by a carbon price in China by then, the levy to import them into the EU should be correspondingly lower.

Indeed, the impending CBAM has spurred action on carbon pricing in countries not otherwise known for their climate policy ambition.

Several of the EU’s trading partners – whose products could be affected by the carbon levy – are exploring carbon taxes, emissions trading systems, and other measures that would negate the need for a border adjustment because the country in which the product is made already puts a price on the emissions that production caused. These include Turkey, Morocco, Indonesia, and Vietnam.

Competitiveness concerns

These countries are concerned for the very same reason the EU came up with the idea of a CBAM in the first place: levelling the playing field.

Our survey reflects a rising concern among European companies covered by the EU ETS that their products will lose market share relative to competitors not subject to carbon prices in their home country.

Views on this have shifted markedly in recent years. While 63 percent of the respondents from companies saw the EU ETS as “detrimental” or “somewhat important” to their competitiveness back in 2017, a staggering 95 percent of the respondents held that view in 2021 – and all of them did in 2022.

On the flip side, not a single respondent to this year’s survey has moved its business outside the EU due to carbon costs and only one is considering doing so. This represents the largest-ever share of respondents who declared the cost of emitting greenhouse gases in Europe will not make them leave.

Interest in voluntary carbon markets on the rise

Beyond these expectations for compliance markets, our survey’s findings reflect strong growth expectations for the voluntary carbon market (VCM), where corporate entities or individuals offset their emissions by purchasing carbon reduction units (offsets) to meet carbon neutrality targets.

In 2021, new records were set both in volumes and values in the voluntary market. Turnover hit an all-time high annual value of $1 billion in late 2021 and a record 300 million tonnes were traded.

Over 70 percent of the respondents to our survey assume that 2022-2023 volumes will be even higher, despite the global energy and commodity crises caused by the war in Ukraine.

As far as which “carbon credits” corporate buyers want, the survey results indicate that the standard to which the offset units being traded are certified matters most in buyers’ voluntary market purchasing decisions.

Asked which factors influence their choice of offsets, the vast majority (73 percent) of respondents cited the unit’s respective certification or standard, followed by project type (64 percent), and project location (59 percent).

It’s important to keep in mind that the VCM is a small market compared with the compliance carbon markets set up by governments.

Voluntary trading is still mostly over-the-counter, and transactions are reported somewhat arbitrarily despite great efforts by exchanges and aggregators to standardise both offset credits and transactions.

Other mandatory ETS run by countries like South Korea and New Zealand have larger turnover than the global voluntary market, but did not feature prominently in our survey results due to their low response rate.

Keeping tabs on carbon markets entails watching these compliance markets, which have the backing of national governments, over the so far less accountable offsetting efforts of companies making carbon neutrality and net-zero claims.

Ultimately, carbon markets – compliance or voluntary – exist for the same reason; namely to channel investments from black and grey to green so that emissions are reduced to help meet the Paris Agreement climate ambition.