Analysis of looming downturn amid tightening bank credit, a lack of new debt and high cash buffers following extensive government COVID support while the junk bonds continue to remain calm. The blog explores market risks and concerns as bank credits crunch and global recession fears grow.

- Junk bond remains calm amidst looming recession fears owing to number of factors including the lack of new high yield debt sales this year due to the funding hiatus in the bank sector and availability of growing private credit funds to offset refinancing stress or higher credit standards, albeit at relatively expensive levels.

- But they ultimately see the market coming unstuck later in the year with “decompression and material spread widening” that could force U.S. junk spreads to almost double to a whopping 860 basis points by year-end.

- Bank of America talks about the “consensus lust” for a recession in showing a net 63% of the global fund managers it polled this month seeing a weaker economy ahead – the highest this year so far.

For more data-driven insights in your Inbox, subscribe to the Refinitiv Perspectives weekly newsletter.

LONDON, April 19 (Reuters) – If a mega Western recession is coming down the pike in the second half of this year, someone should point it out to the junk bond market.

The investment herd seems more convinced than ever that recession is on the way amid tightening bank credit after the March bank stress – even if not all the incoming evidence supports that take.

But in the light of that level of bearishness alone, the extraordinary relative calm in the riskier part of the corporate debt world is a bit of a head-scratcher.

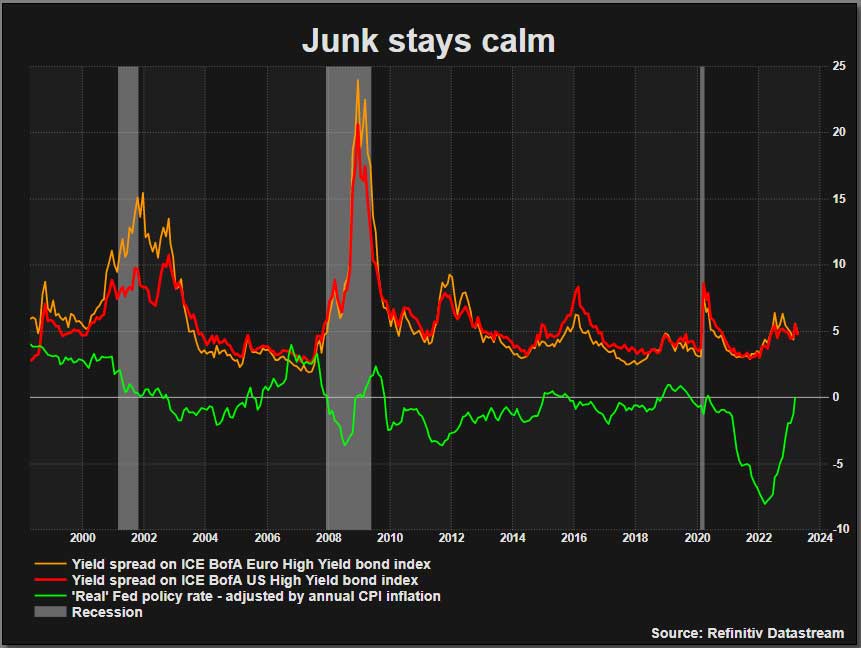

At less than 5 percentage points, the risk premium on the broadest five-year U.S. and European high-yield bond indexes are more than half a point lower than the peak of the March bank drama. But zoom out a bit and you’d hardly detect the disturbance of the past six weeks on a 25-year chart.

Current yield spreads are more than a full point lower than last year’s peaks, when the Federal Reserve was ratcheting interest rates higher. They’re almost half the pandemic peaks and a fifth of the great financial crisis 15 years ago.

A lack of new debt and high cash buffers following extensive government COVID support is a big part of the story. And junk spread jumps tend to be coincident with recession rather than a leading indicator.

But even so, the pricing is still remarkable against such overwhelming surety among asset managers about the looming downturn.

Refinitiv news service: The exclusive provider of Reuters News to the financial community

Weaker economy ahead

Bank of America talks about the “consensus lust” for a recession in showing a net 63% of the global fund managers it polled this month seeing a weaker economy ahead – the highest this year so far. More than a third now see the biggest risk ahead as a bank credit crunch and global recession.

And the respondents claim to be putting their money where their mouths are, with the largest overweight bond position and biggest underweight real estate positioning since 2009.

But while up to their collective neck in cash and investment grade bonds, almost half of all funds – the most on record – reckon investment grade credit will outperform junk bonds over the next 12 months. And that’s with junk spreads more than three times higher than quality corporates.

Hardly surprising with S&P Global credit rating firm expecting U.S. high-yield default rates to more than double to an admittedly still-modest 4% by the end of this year and with more than half a trillion dollars of floating rate debt among credits rated B-minus or lower.

Deutsche Bank’s credit team on Tuesday said they saw U.S. high-yield default rates tripling to as high as 9% by the end of next year, and leveraged loan rates rising almost fivefold to more than 11%.

Courage and decompression

There’s little doubt that many investors want to steer well clear, for now at least.

“I’m not courageous enough to get involved in high yield yet – especially the lower rated part,” said Stephane Monier, Chief Investment Officer at Lombard Odier’s private bank, explaining his overweight cash and investment grade bond position alongside an overweight in Chinese equity.

“I’ve been managing credit for 30 years and never bought high yield before the first defaults in that cycle – and it’s served me well,” Monier added, pointing to a possible rethink if his expected second-half U.S. recession sees the market repricing on some of the early related company defaults.

And yet an eerie calm in pricing persists.

Not unlike the resilience in broader stock indexes, calm on the surface masks the turbulence in bank funding and some rotation between different segments of credit quality.

It also partly reflects some of the surprisingly strong economic numbers of late that at least question the recession narrative. And at the same time refinancing fears will have been soothed by the outsize swoon in benchmark borrowing costs and U.S. Federal Reserve expectations around the March shock.

But that may be shaky ground for high-yield bonds to balance on as it will be hard to sustain both environments. Many Fed officials, for example, openly question the market “lust” for recession.

“Wall Street’s very engaged in the idea there’s going to be a recession in six months or something, but that isn’t the way you would read an expansion like this,” the hawkish St Louis Fed chief James Bullard told Reuters on Tuesday.

And as Monier points out, you could get a rise in default rates and market repricing without a technical recession in the wider economy.

So, what gives?

Junk bonds to come unstuck later in the year

In a note entitled “Squeeze Before The Storm”, Deutsche’s credit strategist Steve Caprio and team reckon the calm in junk spreads could persist through the spring and early summer, but the lagged impact of central bank tightening would kick in eventually this year.

They cite a number of factors for seeming serenity, including the lack of new high-yield debt sales this year due to the funding hiatus in the bank sector and also the availability of growing private credit funds to offset refinancing stress or higher credit standards, albeit at relatively expensive levels.

But they ultimately see the market coming unstuck later in the year with “decompression and material spread widening” that could force U.S. junk spreads to almost double to a whopping 860 basis points by year-end.

Refinitiv news service: The exclusive provider of Reuters News to the financial community

The opinions expressed here are those of the author, a columnist for Reuters.