While stock markets in the U.S. and Europe surge to new highs in the face of rising COVID-19 cases, emerging market equities have been more subdued. September’s Market Voice analyses the reasons behind this, and considers the prospect for a future rally in emerging markets.

- In spite of rising cases of COVID-19 and inflationary pressures, U.S. stocks continue to hit new highs. European markets have also been buoyant.

- However, there is less of a correlation between emerging market equities and COVID-19 cases.

- Central banks in emerging markets are sensitive to inflationary pressures and respond by hiking interest rates. Should central banks in developed markets hike interest rates, this may cause a consequent rally in emerging market equities.

For more data-driven insights in your Inbox, subscribe to the Refinitiv Perspectives weekly newsletter.

The U.S. stock market is no longer subject to the laws of gravity.

As shown in Figure 1, with each passing day the SPX makes new highs seeming to shrug off negative news: surging inflation, gaping fiscal deficits, potential mass evictions and the delta variation of COVID-19. But the SPX stellar performance is not carrying over to all global markets.

While emerging market (EM) equities outperformed the SPX in the early months of the pandemic, they peaked in February and then retraced more than 8 percent. In the November 2020 Market Voice, we assessed that EMs were benefiting from COVID-19’s delayed spread (at least based on local reporting) in EM nations and they were less capable of enforcing the draconian economic shutdowns adopted in developed nations.

In addition, many emerging markets entered the pandemic with positive interest rates so, unlike the industrial world where rates were largely at or below zero, EM central banks had latitude to cut rates.

Figure 1: Morgan Stanley Emerging Market Index diverges From the S&P

Refinitiv Eikon gives you the information you need – whenever and however you want it

U.S. and European markets strong in spite of COVID-19

In the November piece, we anticipated that EM countries would eventually have negative repercussions from their inability to impose shutdowns and this is consistent with the subsequent outperformance of the U.S. market. But the variation in market performance is not limited to emerging markets.

As shown in Figure 2, the European markets remain highly correlated with the U.S. market; the STOXX, like the SPX, has been steadily making new highs. Correlation between the Nikkei and the SPX, however, has trended lower all year. Like EM markets, the Nikkei peaked out in the first quarter but then moved into a sideways pattern avoiding a steep pullback.

Figure 2: S&P 3-month correlation with emerging markets, Europe and Japan

It is tempting to conclude U.S. and European outperformance reflects relative success at containing the spread of COVID-19, but Figure 3 suggests the story may be more complicated.

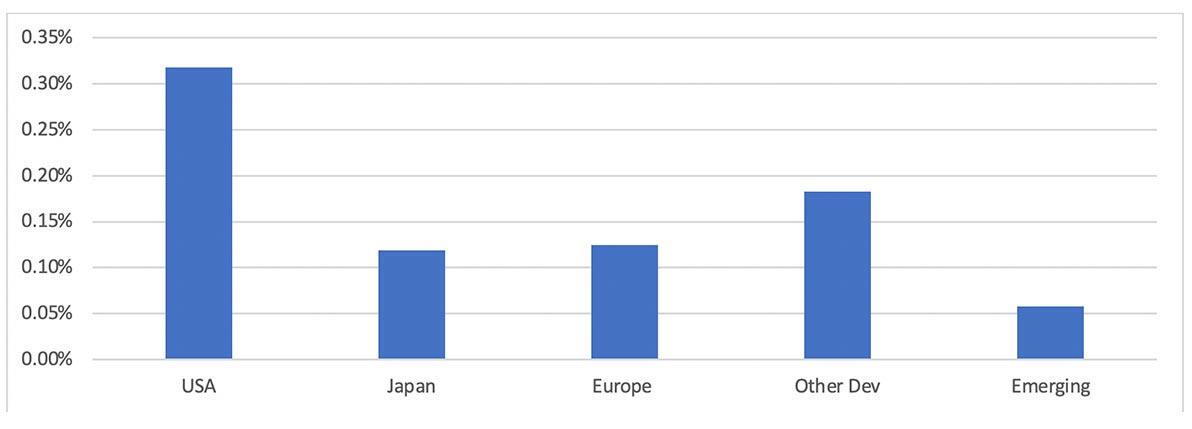

The U.S. had a higher pace of new COVID-19 cases per population during August than other regions of the world. Japan had a significantly lower new case rate than either the United States or Europe, which seems inconsistent with the underperforming Nikkei. And emerging markets continue to see a much slower pace of new cases than the developed world.

So what is causing the stronger performance of the U.S. market?

Figure 3: August weekly COVID-19 cases a percentage of populate

Figure 4: Y/Y change (through August) equity market vs number of new COVID -19 cases

Source: Eikon

Source: Eikon

Economic impact of lockdowns

Part of the discrepancy between new case levels and market performance may be variations across countries at their accuracy of data collection.

Perhaps more important is that the shutdown response and consequent economic impact varied, potentially distorting the connection between case levels and market performance.

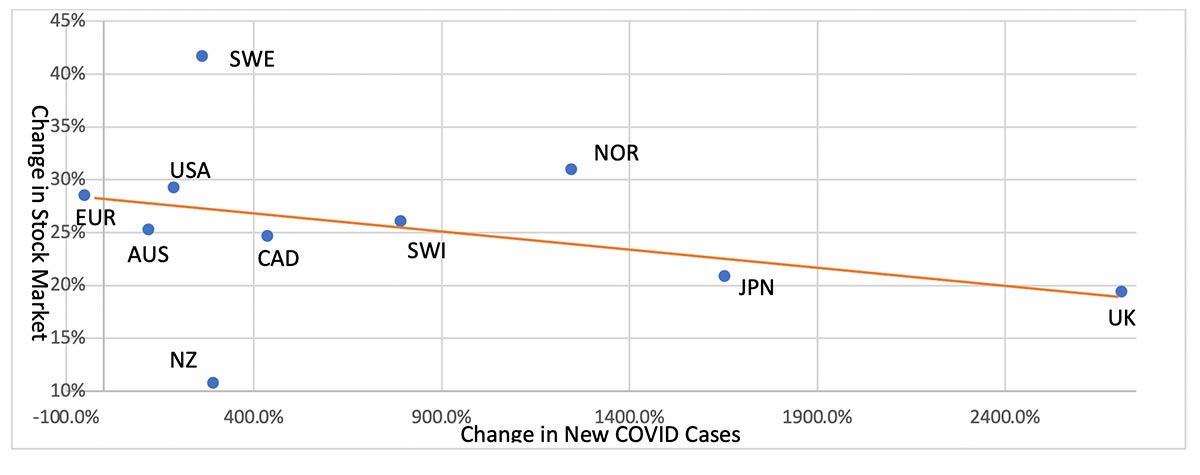

Figure 4 above, compares stock market performance and the percentage growth in the number of new cases for August of this year from a year earlier. While there are a few outliers – New Zealand on the downside and Norway and, especially, Sweden on the upside – there does appear to be a relationship between the growth in caseload and gains in stock market performance.

The growth of caseload is apparently more important than the total number of people infected for market performance.

Also based purely on the relationship shown above, the New Zealand market appears to be under-priced and Sweden overpriced. The New Zealand underperformance likely reflects the particularly onerous lockdown measures introduced there over the summer in an attempt at total elimination of COVID.

Figure 5: Growth in COVID-19 vs stock market performance over past six months

Impact of COVID-19 on emerging markets

The relationship between COVID-19 case growth and market performance is less robust for emerging markets.

One problem is that some emerging markets were reporting only a handful of cases a year ago, so even a modest rise in absolute terms translates into thousands of percent.

Because of the high variation of COVID-19 appearance in different countries, we limited the look back to six months instead of one year. Even then, some countries – e.g., Thailand – were only reporting a handful of cases so the comparison is limited to countries with case growth rates under 600 percent.

Even with these adjustments, the relationship between growth in cases and market performance, shown in Figure 5 above, is less clear than for the developed countries.

Another factor, however, that may be limiting gains in EM stocks is that the interest rate picture is now largely reversed from a year ago.

Are inflationary pressures a factor?

The Fed has indicated it is considering cutting back on quantitative easing in response to the surge in U.S. inflation to multi-decade highs, but it has yet to take any action. And the Fed has made it clear it does not anticipate hiking rates until at least a year from now.

The market has shown little concern over the Fed’s lack of monetary constraint because of the evidence the Fed has provided that the inflationary pressures are a temporary by-product of panacea supply chain disruptions and should gradually dissipate.

The Fed also has the institutional credibility that a forceful response will be forthcoming if evidence emerges that inflationary pressure is not transitory.

Watch: Eikon – The ultimate set of tools for analysing financial markets

Most countries are feeling the impact of COVID-19-related supply disruptions creating shortages and rising price levels But many EM countries have had more recent history of high inflation and their central banks do not enjoy the credibility and institutional independence of the Fed.

Unlike the Fed, central banks in emerging markets have been forced to be more responsive to higher inflation.

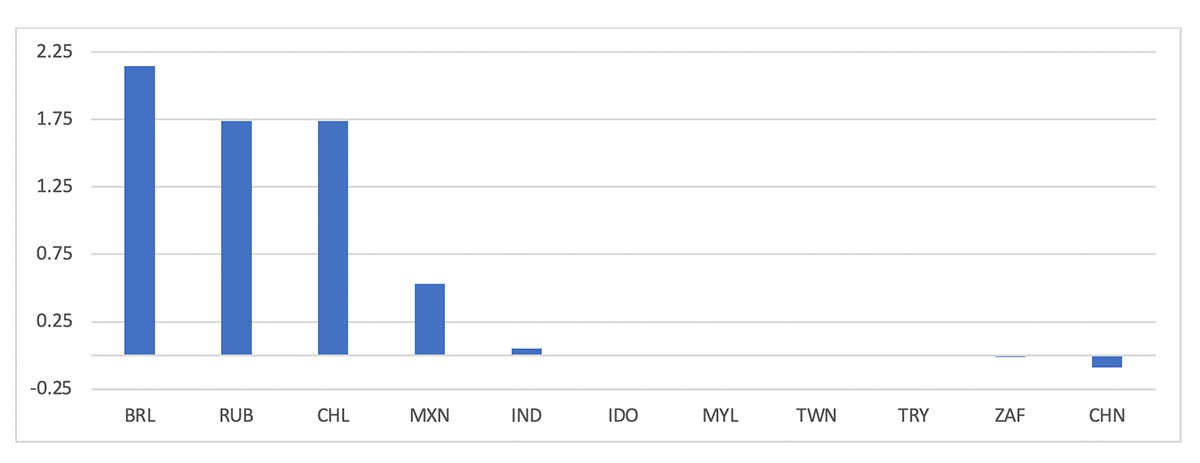

As shown in Figure 6, rates are no longer trending lower in the EM markets and some central banks are already actively hiking. No doubt, this is a factor in the lagging performance of emerging market stocks setting the stage for a catch-up rebound once the developed country central banks finally move to tighten monetary conditions.

Figure 6: Change in on-shore 3-month rates since the end of May

Refinitiv Eikon gives you the information you need – whenever and however you want it