A Refinitiv whitepaper explores the impact that alternative data sets can have on portfolio performance and assesses how a quantitative framework can be used to calculate the monetary value of the sets.

- The research provides an illuminating framework for assessing the added value of alternative data with respect to any benchmark, be it a passive index or an active, factor-based investment strategy.

- As a standalone signal, alternative data matched or out-performed multi-factor strategies and the S&P benchmark.

- The research exemplifies the significant benefits of incorporating alternative data sources into quantitative investing strategies and how alternative data, can increase returns further.

For more data-driven insights in your Inbox, subscribe to the Refinitiv Perspectives weekly newsletter.

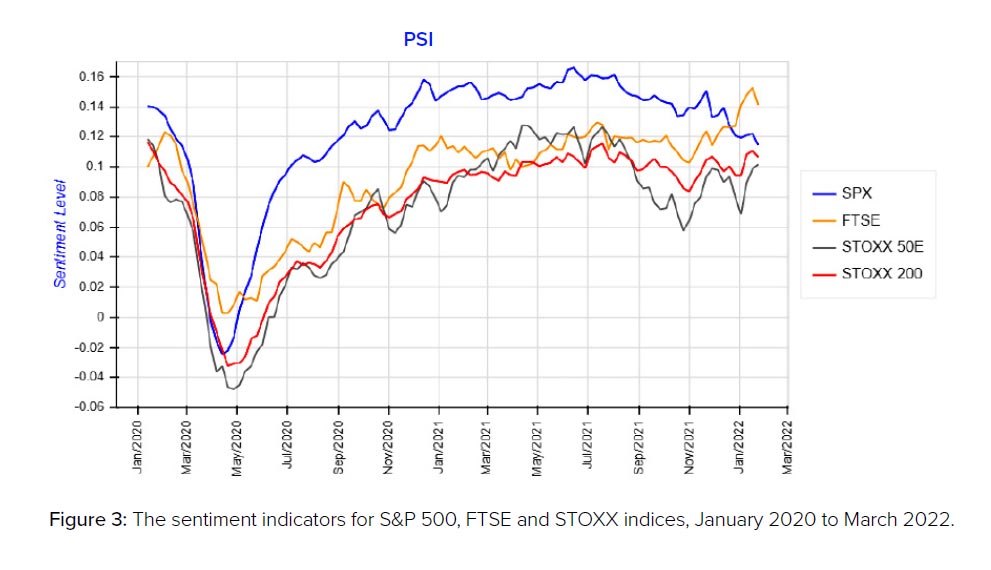

From satellite imagery to media sentiment, the popularity of alternative data continues to grow as investors strive to find a competitive edge. But will the costs of acquiring and managing that data be returned? And how can you award it a monetary value to make a case for its use?

Our latest whitepaper, The value of alternative data: The case for media sentiment, answers these questions.

The study uses backtesting to compare the performance of portfolios when using Refinitiv Media Sentiment as a standalone investment signal, versus a traditional multi-factor strategy or the S&P500 benchmark.

It compares performance across various investor profiles, such as long-only versus long-and-short investors, and monthly versus quarterly rebalancing frequencies.

Read the whitepaper: The value of alternative data: the case for media sentiment

What are the key findings?

1. As a standalone signal, alternative data matched or out-performed multi-factor strategies and the S&P benchmark

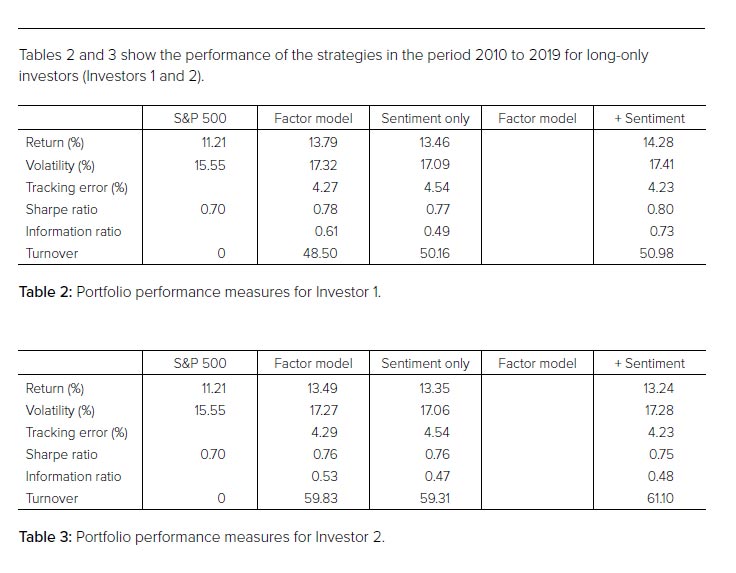

While the results varied between portfolios, overall the study showed that using the alternative data set of media sentiment as a single-factor investment strategy achieved results across return, volatility and the Sharpe ratio on a par with those achieved when using a multi-factor strategy.

For long-only investors, both the multi-factor and sentiment-only strategies delivered between 2 percent and 2.5 percent excess return over the S&P benchmark.

And when tested on long-short portfolios, the sentiment-only strategy even began to outperform the multi-factor model.

These results suggest investors could potentially maximise returns with simpler strategies – making savings on time and resource without sacrificing alpha.

2. Short positions contributed significantly to excess returns over the benchmark – and even the multi-factor model

In the study, the alternative data strategy delivered excess returns over the S&P benchmark of between 3 percent and 5.5 percent for long-short portfolios (compared to 2 percent and 2.5 percent for long-only).

And when the portfolios were made up of 50 percent or more short positions, the sentiment-only strategy began to outperform both the benchmark and the multi-factor strategy.

In this case, the higher the short percentage, the higher the returns – and the more beneficial the sentiment-only strategy over the multi-factor model and benchmark.

3. Multiplying the fund AUM by the GH1 measure is an effective way to quantify the monetary value of alternative data strategies

To answer the question of how to calculate the monetary value of alternative data sets, the whitepaper sets out a quantitative framework.

This consists of calculating the GH1 measure for each portfolio with respect to either a benchmark or multi-factor strategy, and then multiplying that measure by the fund’s AUM to give an expected additional yearly income for the fund when using an alternative data set.

For example, for one hypothetical investor in the study, the sentiment-only strategy GH1 metric with respect to S&P500 was equal to 1 percent per annum.

For a fund of US$100M, this would equate to a US$1M profit per year. And when compared against the multi-factor strategy, the same investor achieves a GH1 measure of 0.42 percent, equal to US$420K additional profit.

Calculated against recovery factors this provides a useful guide for evaluating the real value of the data, and making a compelling case for its use.

4. The value of alternative data extends beyond direct alpha returns

Calculating a monetary figure for additional returns is just one way to evaluate value.

The study takes the position that a comprehensive valuation framework for alternative data should consider both return enhancement and risk reduction.

This is because by decreasing volatility – as demonstrated in some of the backtests – alternative data can still give the opportunity to increase returns. This is particularly true if the reduction in volatility is dramatic (as detailed in an example given in the whitepaper).

5. Combining alternative data with more complex models may increase returns further

The examples given and strategies used in the whitepaper are simple, and the real value of any alternative data will depend on the investor profile and the fund size.

The whitepaper showed that adding the alternative data set to an existing multi-factor strategy further increased returns and improved the Sharpe ratio. It, therefore, warrants further exploration to see whether using a dataset like media sentiment in combination with more sophisticated strategies could deliver even better returns.

Understand more about the value of alternative data

To understand more about the methodology, findings and the quantitative framework for evaluating the value of alternative data, download the whitepaper.

The whitepaper explores how the long-only and long-short portfolios performed, as well as provides insights into the impact on the Sharpe ratio and turnover.

Read the whitepaper: The value of alternative data: the case for media sentiment