A recent whitepaper from Probability & Partners and Refinitiv analyses the results of combining sustainable and multifactor investment strategies. It found that adding sustainable investing considerations to multifactor investment strategies does not materially reduce performance.

- Sustainable and multifactor investing strategies are finding favour in asset management.

- Refinitiv research considers three ways in which ESG metrics can be incorporated in multifactor strategies.

- Sustainability as a risk overlay and/or for sector rotation delivers strong annual returns.

For more data-driven insights in your Inbox, subscribe to the Refinitiv Perspectives weekly newsletter.

Sustainable investing is escalating at speed, driven by millennials and shaped by increasing regulation requiring transparency and disclosure of sustainable investments – essentially Environmental, Social and Governance (ESG) investments. In parallel, factor investing is maintaining traction, with multifactor investment strategies showing strong performance.

While sustainable and multifactor investment strategies are independently gaining momentum among asset managers, the whitepaper from Probability & Partners and Refinitiv explores the intersection of these strategies in terms of portfolio performance. It specifically addresses two questions:

- Can sustainability be treated as an investment factor?

- What is the impact of sustainability as a screening overlay and as the weighting criteria in sector rotation on the financial performance of multifactor portfolios?

How can you incorporate Refinitiv ESG data into your investment decision making process?

Methodology of the analysis

Data used in the research for the whitepaper included the returns of S&P 500 and STOXX 600 historical stocks from July 2007 to December 2020. Sustainability metrics were provided by Refinitiv Combined Environmental, Social and Governance (ESGC) scores for the same companies and historical period.

The risk-free rate for the S&P 500 stocks was the three-month Treasury Bill and for the STOXX 600 stocks the three-month Euro yield.

The factor model included market, size, growth, momentum and volatility factors, with factor portfolios constructed using the Fama & French approach.

The research considered three ways in which ESG metrics can be incorporated in multifactor strategies.

What were the results?

Factor portfolio

Research into the addition of a specific factor based on ESG scores to a multifactor strategy answers the whitepaper’s first question of whether sustainability can be treated as an investment factor.

The table above shows weekly returns of factor portfolios. The average weekly return of the volatility factor (SMV) and sustainability factor (ESG) is negative for both the S&P 500 and STOXX 600. This suggests more stable stocks underperform volatile stocks and sustainable stocks underperform less sustainable stocks.

The size (SMB) and momentum (WAL) factors show positive returns, reflecting interest in factor investing.

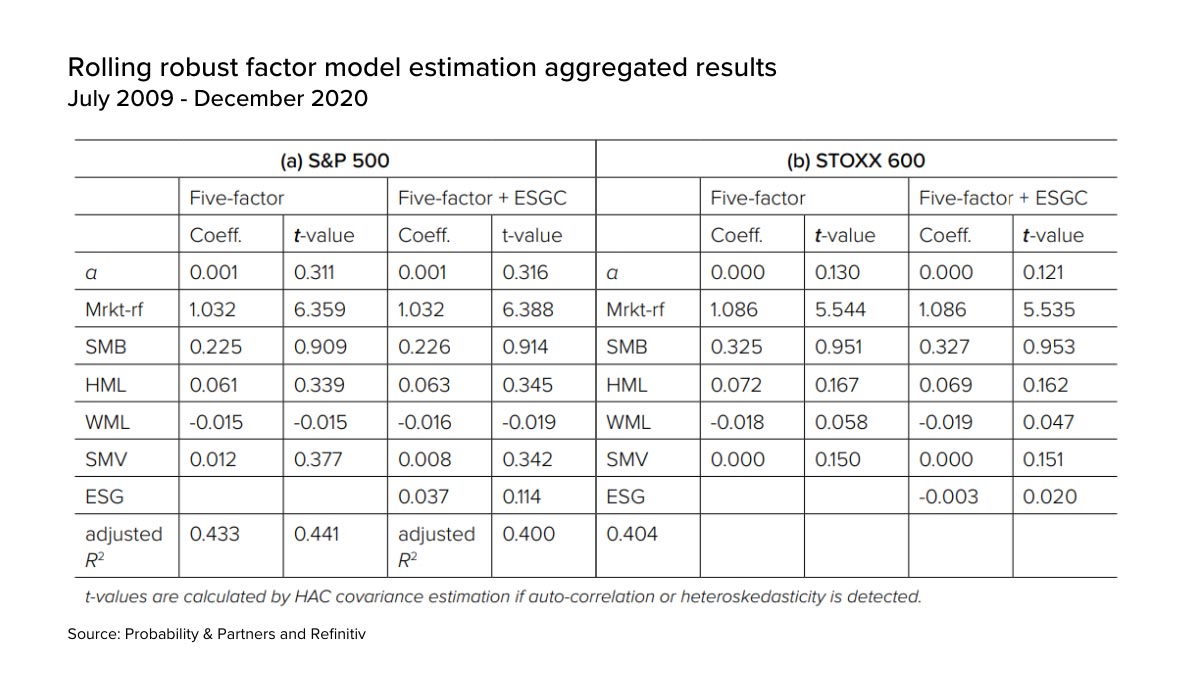

The table above presents aggregated results for investment models with and without the sustainability factor, and shows that the factor is not significant in either the S&P 500 or STOXX 600 universe.

These results indicate that sustainability as a factor does not contribute performance to a traditional multifactor model.

This is underlined in the table below that shows performance of portfolios based on a five-factor model is similar to that of portfolios based on a five-factor model with the addition of a sustainability factor.

Using ESG scores as a risk overlay and for sector rotation

To answer the whitepaper’s second question of whether sustainability as a screening overlay and as the weighting criteria in sector rotation will have an impact on the performance of portfolios, the research considers the effects of various levels of screening and sector rotation on S&P 500 and STOXX 600 portfolios.

Discover the full results in the Incorporating ESG considerations in multifactor strategies whitepaper.

Conclusion on sustainable investing

The aim of sustainable investment strategies is to take sustainability into investment decision making in a way that achieves a higher sustainability profile in portfolios without sacrificing profit.

This Probability & Partners and Refinitiv whitepaper demonstrates to a great degree that this can be achieved.

The research concludes that sustainability should not be considered as an investment factor in multifactor strategies as it does not make a significant difference to portfolio performance.

Sustainability can, however, be used as a stock screening overlay and/or for sector rotation in multifactor strategies.

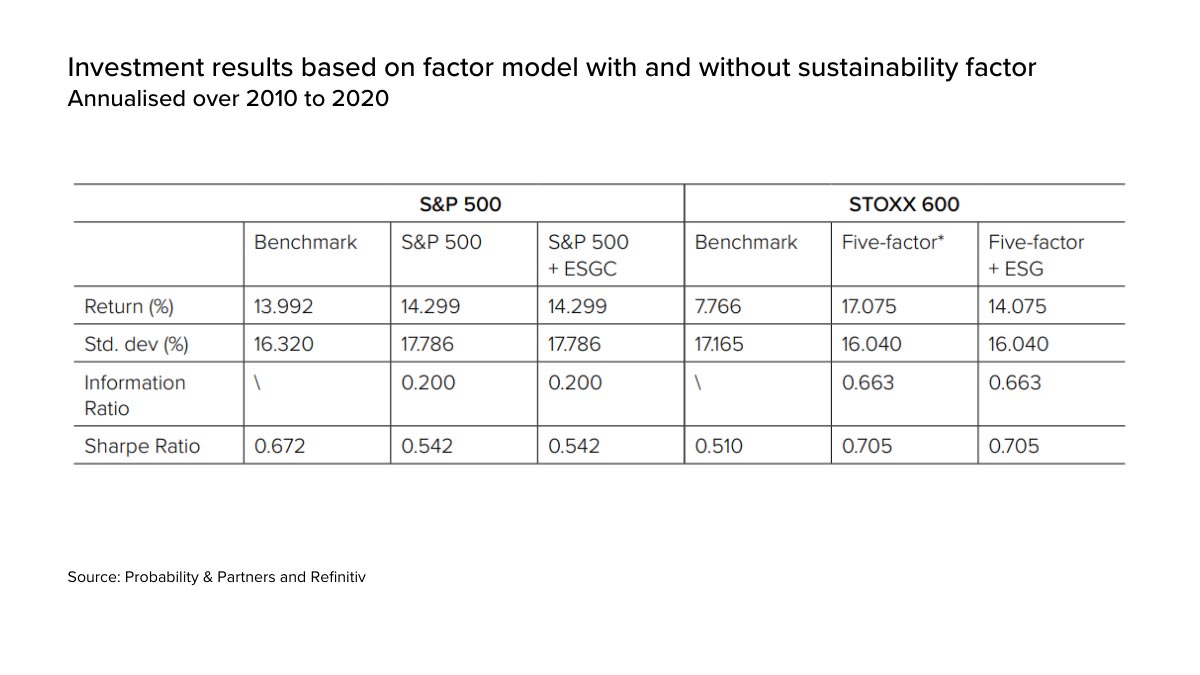

This produces slightly lower performance metrics on occasion, compared with those of unscreened multifactor strategies. However, the trade-off is acceptable as resulting portfolios significantly outperformed the benchmark, and using the most aggressive ESG screening and sector rotation, the S&P 500 delivered an annualised return of 18.5 percent and the STOXX 600 15.3 percent.

A sustainable investment process should, therefore, aim to create a balance between improving the sustainability metrics of a portfolio and the impact this will have on risk and returns.

How can you incorporate Refinitiv ESG data into your investment decision making process?