How can access to more accurate and standardised ESG data, improved disclosure and higher quality and more consistent corporate reporting help to increase sustainable investment?

- Investors need accurate data and better ways to measure to build sustainability into their workflow.

- The majority of asset owners state the lack of standardisation in ESG data, scores and ratings is most common barrier to increased adoption of sustainable investment.

- ESG data, better disclosure and higher standards of corporate reporting will play a crucial role in helping move the financial industry forward.

The sustainable investment revolution is picking up speed.

Issues such as climate change, environmental pollution, biodiversity, human rights, business ethics and corporate governance are now at the forefront of public attention.

More and more investors have signed up to global initiatives, such as the United Nations’ Principles for Responsible Investment (UN PRI), to help cause change in these areas.

However, there’s a stumbling block: inconsistent, low-quality and patchy data. Investors need better data and better ways to measure it in order to build sustainability into their funds and investment products.

What’s wrong with the data?

There’s been a decade-long push to improve standards of environmental, social, and governance-related (ESG) metrics and disclosure across the corporate sector.

In 2015, the G20 Financial Stability Board (FSB) set up an industry-led task force on climate-related financial disclosures (TCFD) to design a better transparency framework.

Its goal, set out in 2017 with the publication of TCFD’s recommendations, was to enable financial market participants to understand better their climate-related risks.

In October 2021 the TCFD issued further guidance on disclosures of climate-related metrics, using FTSE Russell’s carbon targets framework as an example of transparency on corporate greenhouse gas emissions reduction targets.

Recent European Union initiatives – such as the 2016 Benchmark Regulation, the 2020 Taxonomy Regulation and the 2021 Sustainable Finance Disclosure Regulation – all show the growing commitment of policymakers in the area of sustainability.

But ensuring that extra-financial disclosures catch up with mandatory financial reporting is a tough challenge. And it’s one where the industry is still falling short, according to many observers.

“Gaps in ESG metrics continue to make it difficult for investors to compare the sustainability performance of different companies,” say David Harris, Global Head of Sustainable Finance, London Stock Exchange Group, and Arne Staal, CEO, FTSE Russell.

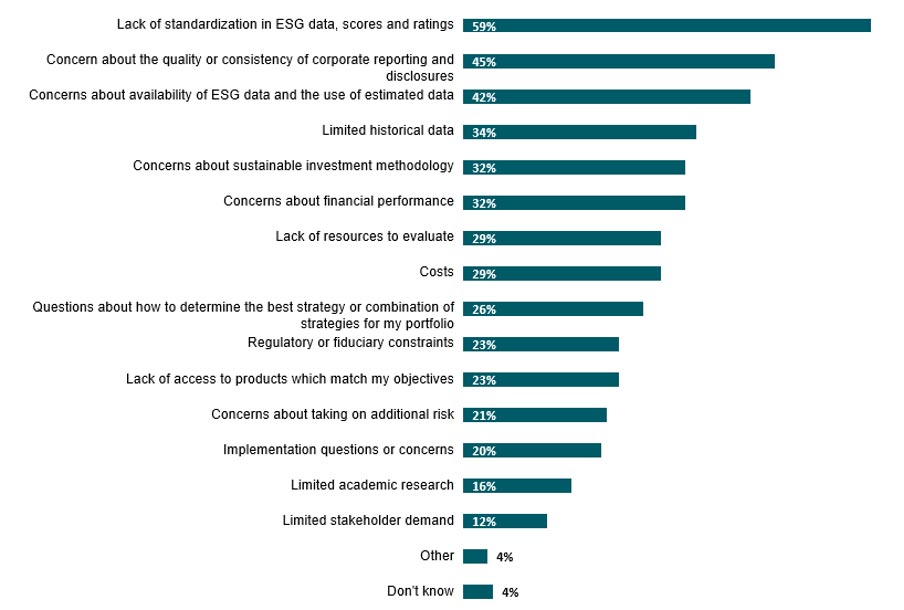

Poor data a barrier to sustainable investment

According to the 2021 FTSE Russell asset owner survey, which researched almost 200 global asset owners, the lack of standardisation in ESG data, scores and ratings is the most commonly cited barrier to the increased adoption of sustainable investment, with 59 percent of survey respondents stating this as their primary concern.

Almost half (45 percent) of survey respondents expressed concern about the quality or consistency of corporate reporting and disclosures, while 42 percent are concerned about the availability of ESG data and the use of estimated data.

Perceived barriers to sustainable investment adoption

Doubts over data standards help fuel allegations of ‘greenwashing’ – cheating on sustainability –at companies and investment product providers.

The need for transparency and objectivity

Transparency is a necessary first step in ensuring that sustainability/ESG data is fit for purpose.

It is critical in driving accurate investor information, public discourse and regulatory guidance. Transparency also helps to achieve positive outcomes both within finance and across society.

The investment solutions businesses of the London Stock Exchange Group (LSEG), FTSE Russell and Refinitiv, collect and use data that is publicly disclosed. This means it is possible to audit the data all the way from public documents (such as annual reports) to the resulting company scores and fund ratings.

In addition, sustainability data should be measured as objectively as possible, which is not an easy task. Early ESG databases tended to focus on companies’ operations, rather than their products, services or supply chains.

It’s hard to expect companies to be able to report on the broader social and environmental impact of their products and services in as objective and measurable way as they report on their own activities, but this is a goal capital market participants need to set themselves.

The EU’s new Taxonomy for sustainable activities, which requires companies to report on the proportion of revenues, and operational and capital expenditures that are ‘green’, is likely to be an important first step in ensuring the comparability of corporate sustainability data.

FTSE Russell’s Green Revenues data model and Classification System, launched in 2015, offered an early example of how to do this: it goes beyond the traditional focus on how a company operates and measures that company’s green revenues in terms of products and services.

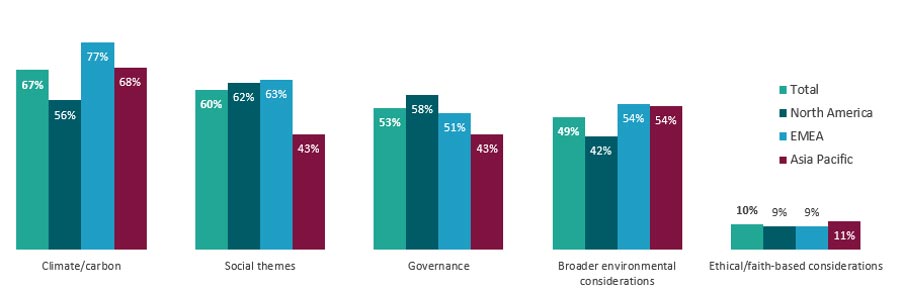

There’s increasing societal pressure to arrive at better standards in this area. For example, over two-thirds of the asset owners who participated in the annual FTSE Russell survey say that climate and carbon are their priority focus area when seeking to invest sustainably.

Sustainability issues of priority focus

But compare that demand with the current state of affairs, where only half of the companies in Refinitiv’s ESG database currently report on CO2 emissions. As a result, Refinitiv has developed sophisticated carbon models based on a transparent methodology.

These provide clients with an estimated carbon emissions value when a reported value is not available.

Better sustainability data opens the door for asset managers and asset owners to employ a range of new applications to mitigate risk and generate performance.

For example, MarketPsych ESG Analytics extract complex meaning from the text of millions of articles and social media posts. This is summarised into a single score, offering a near-real time measurement of a company’s or country’s sustainability.

Two-way communication on sustainability

Improved information flows between asset owners and investee companies could also help reinforce the trend towards sustainable investing.

Asset owners and asset managers may wish to tell companies which metrics they prioritise and wish to assess, while corporations can play their own role in ensuring the supply of transparent, accurate and comparable sustainability/ESG data for the financial industry.

Refinitiv’s ESG Contributor Tool allows corporate managers to review, update and publish their firms’ ESG data within the Refinitiv ecosystem. Almost 1,000 contributors have accessed the tool.

This ensures data users have access to the timeliest data on individual companies, as well as allowing those supplying information to check its quality and comparability.

Paths towards sustainable investment

As world leaders gathered in Glasgow for the 26th United Nations conference on climate change, there’s increasing pressure on politicians, business leaders and policymakers to follow scientists in setting out a path towards more sustainable development.

Many factors will play a role in determining the success of this important and long-awaited event. But improved ESG data, better disclosure and higher standards of corporate reporting will play a crucial role in helping move things forward.

© 2021 London Stock Exchange Group plc and its applicable group undertakings (the “LSE Group”). The LSE Group includes (1) FTSE International Limited (“FTSE”), (2) Frank Russell Company (“Russell”), (3) FTSE Global Debt Capital Markets Inc. and FTSE Global Debt Capital Markets Limited (together, “FTSE Canada”), (4) MTSNext Limited (“MTSNext”), (5) Mergent, Inc. (“Mergent”), (6) FTSE Fixed Income LLC (“FTSE FI”), (7) The Yield Book Inc (“YB”) and (8) Beyond Ratings S.A.S. (“BR”). All rights reserved.

FTSE Russell® is a trading name of FTSE, Russell, FTSE Canada, MTSNext, Mergent, FTSE FI, YB and BR. “FTSE®”, “Russell®”, “FTSE Russell®”, “MTS®”, “FTSE4Good®”, “ICB®”, “Mergent®”, “The Yield Book®”, “Beyond Ratings®” and all other trademarks and service marks used herein (whether registered or unregistered) are trademarks and/or service marks owned or licensed by the applicable member of the LSE Group or their respective licensors and are owned, or used under licence, by FTSE, Russell, MTSNext, FTSE Canada, Mergent, FTSE FI, YB or BR. FTSE International Limited is authorised and regulated by the Financial Conduct Authority as a benchmark administrator.

All information is provided for information purposes only. All information and data contained in this publication is obtained by the LSE Group, from sources believed by it to be accurate and reliable. Because of the possibility of human and mechanical error as well as other factors, however, such information and data is provided “as is” without warranty of any kind. No member of the LSE Group nor their respective directors, officers, employees, partners or licensors make any claim, prediction, warranty or representation whatsoever, expressly or impliedly, either as to the accuracy, timeliness, completeness, merchantability of any information or of results to be obtained from the use of FTSE Russell products, including but not limited to indexes, data and analytics, or the fitness or suitability of the FTSE Russell products for any particular purpose to which they might be put. Any representation of historical data accessible through FTSE Russell products is provided for information purposes only and is not a reliable indicator of future performance.

No responsibility or liability can be accepted by any member of the LSE Group nor their respective directors, officers, employees, partners or licensors for (a) any loss or damage in whole or in part caused by, resulting from, or relating to any error (negligent or otherwise) or other circumstance involved in procuring, collecting, compiling, interpreting, analysing, editing, transcribing, transmitting, communicating or delivering any such information or data or from use of this document or links to this document or (b) any direct, indirect, special, consequential or incidental damages whatsoever, even if any member of the LSE Group is advised in advance of the possibility of such damages, resulting from the use of, or inability to use, such information.

No member of the LSE Group nor their respective directors, officers, employees, partners or licensors provide investment advice and nothing contained in this document or accessible through FTSE Russell Indexes, including statistical data and industry reports, should be taken as constituting financial or investment advice or a financial promotion.

Past performance is no guarantee of future results. Charts and graphs are provided for illustrative purposes only. Index returns shown may not represent the results of the actual trading of investable assets. Certain returns shown may reflect back-tested performance. All performance presented prior to the index inception date is back-tested performance. Back-tested performance is not actual performance, but is hypothetical. The back-test calculations are based on the same methodology that was in effect when the index was officially launched. However, back- tested data may reflect the application of the index methodology with the benefit of hindsight, and the historic calculations of an index may change from month to month based on revisions to the underlying economic data used in the calculation of the index.

This publication may contain forward-looking assessments. These are based upon a number of assumptions concerning future conditions that ultimately may prove to be inaccurate. Such forward-looking assessments are subject to risks and uncertainties and may be affected by various factors that may cause actual results to differ materially. No member of the LSE Group nor their licensors assume any duty to and do not undertake to update forward-looking assessments.

No part of this information may be reproduced, stored in a retrieval system or transmitted in any form or by any means, electronic, mechanical, photocopying, recording or otherwise, without prior written permission of the applicable member of the LSE Group. Use and distribution of the LSE Group data requires a licence from FTSE, Russell, FTSE Canada, MTSNext, Mergent, FTSE FI, YB and/or their respective licensors.