Geordie Wilkes analyses the key trends in the coffee market during the first quarter of 2021, as demand increases following the COVID-19 pandemic.

- Consumer demand for coffee is rising at major airports and shopping locations, presaging a general performance improvement in the coffee market.

- The heightened unemployment among young people caused by COVID-19 could affect demand for coffee.

- Estimates of low crop yields for Brazil may impact the supply, and consequently price, of coffee for the next two to three years.

For more data-driven insights in your Inbox, subscribe to the Refinitiv Perspectives weekly newsletter.

The coffee market has performed well this year, and is up 40 percent YTD at the time of writing.

This improvement is because of an off-year crop cycle and a strong resumption from the demand side of the equation. During the COVID-19 pandemic, while no consumption was lost in the calendar year, demand did not grow as the market shifted heavily to at-home consumption. This has been confirmed by earnings reports from Nestle, Starbucks, and JDE.

Coffee market begins recovery

As economies re-open, out-of-home consumption is starting to recover, and we see global hotspots for coffee consumption such as airports, shopping malls, and key business regions, such as the City of London, benefit the most.

The Pret Index created by Bloomberg outlines the transactions at Pret A Manger Ltd at airports in London and New York, as well as major shopping locations in London, Hong Kong and New York. The index saw sales in stores rise by 20 percent in the week to 29 July.

The index works on a scale of 0 to 1, with 1 being pre-pandemic sales. Every point (0.01) represents 1 percent. London airports reached 0.62 in the week to 19 July, as airports become busier with people looking to get a summer holiday in.

London stations have reached 0.72, up 0.03 on the week, and this suggests an increase in commuting, and internal travel. This is all but confirmed when you look at sales in the West End where the index increased to 0.77. London suburb consumption was at 1.02 as of 29 July, which is in line with expectations that consumption has shifted away from central business districts back to residential areas, due to lockdowns.

Will global unemployment affect demand?

One headwind to demand could be the higher levels of unemployment in the millennial age bracket.

The employment rate for 15-24-year-olds in Q2 2021 in the UK, U.S., and EU are 50.3 percent, 49.8 percent and 30.8 percent respectively, and for the OECD the employment rate is 39.9 percent.

However, demand for coffee is price inelastic and this suggests that as prices rise there will be a limited reduction in demand.

Exports from Brazil have been elevated, until recent months, indicating demand remains strong. The decline in export figures can be attributed to the end of the crop year, fragilities in the shipping industry, high freight prices and entering an off-cycle crop year.

The recent rally has been attributed to a drought and two frosts; this has lowered the crop estimates for the 22/23 season which was meant to be an on year.

For reference, in 1975, there was a frost in Brazil, and this caused the NY contract to rally to 333.60cts/lb in 1977. The delay was due to the limited communication channels and data availability. In 1994 when we had a drought, the certs went to 25,000.

How are coffee inventories faring?

Inventories are being propped up by semi-washed coffee that Brazil exported, and Honduran coffee, the majority of which are in Europe, more specifically Antwerp.

Indeed, 1.1445m bags of ICE certified stocks are from Brazil. In our opinion, this coffee will be consumed with Honduras coffee, with its stocks at 846,891 bags, out of a total 2.154m bags, as of 20 August. It does not look like inventories will be replenished for two to three years due to the low Brazil crop estimates, and Central American coffee cannot fill this gap.

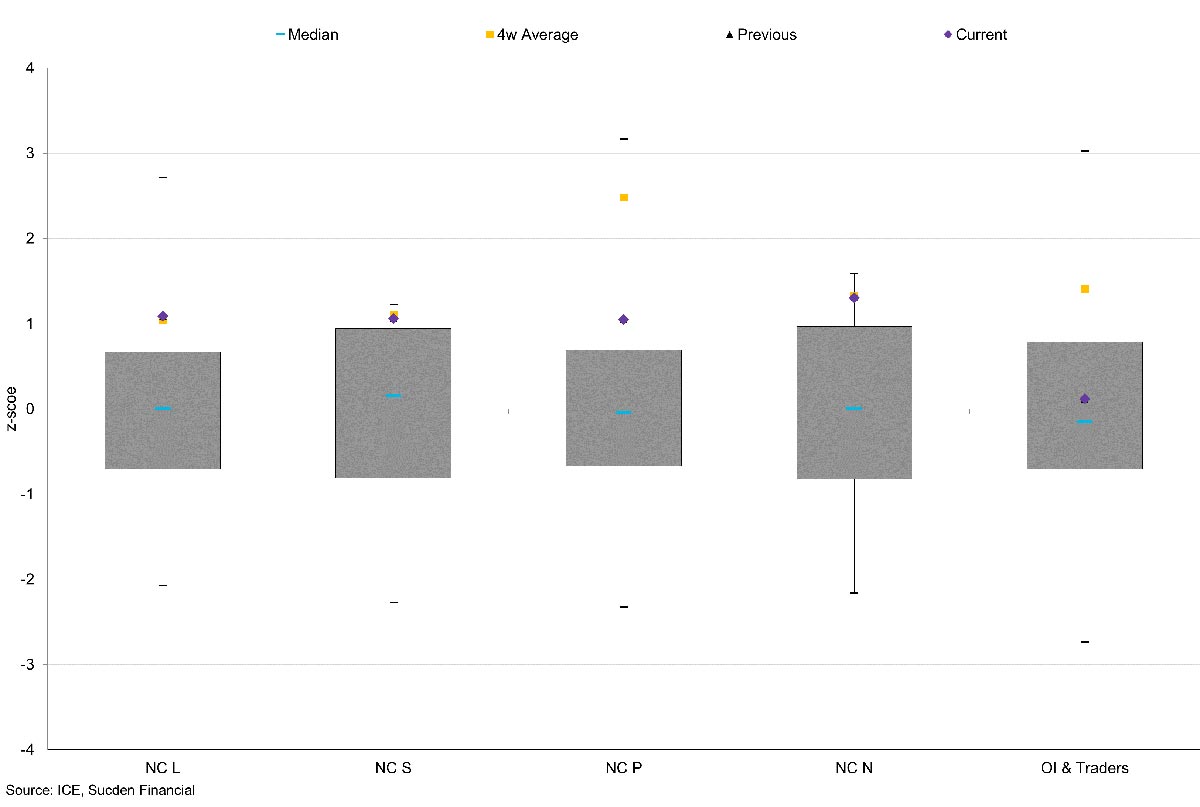

The commitment of traders’ reports indicate that producers hold a 193,666 contract short. They have reduced their position by just over 20,000 after reaching a record short at 218,000 contracts at the beginning of August.

This large gross net short position has been building as producers sold forward to lock in a favourable price. However, as the market rallied, and exchanges increased margin requirements, cracks emerged in this method and it is not inconceivable that some coffee has been sold that isn’t on the trees.

The funds hold a 30,495 contract long and have capacity to add to this position.